VAT was introduced in 1973 due to the UK entering the European Union as a replacement for Purchase Tax and Self Employment Tax. Like purchase tax, VAT is an indirect tax that is charged on consumer expenses. It is levied at all stages of production from raw materials to the finished good and is charged at the point of sale.

There are four categories at which all goods and services may be split into and VAT is charged accordingly. The current 'standard rate' in the UK stands at 17.5%, which is applied to most purchases. Some goods and services have a 'reduced rate' of VAT at 5%, for instance electricity. Certain goods and services are 'VAT exempt', such as health services, rent and insurance. Finally, various products may have a 'zero rate' where they count towards taxable turnover, but have no VAT charges. Examples of such products include children's clothing, books and magazines, prescription drugs and charity.

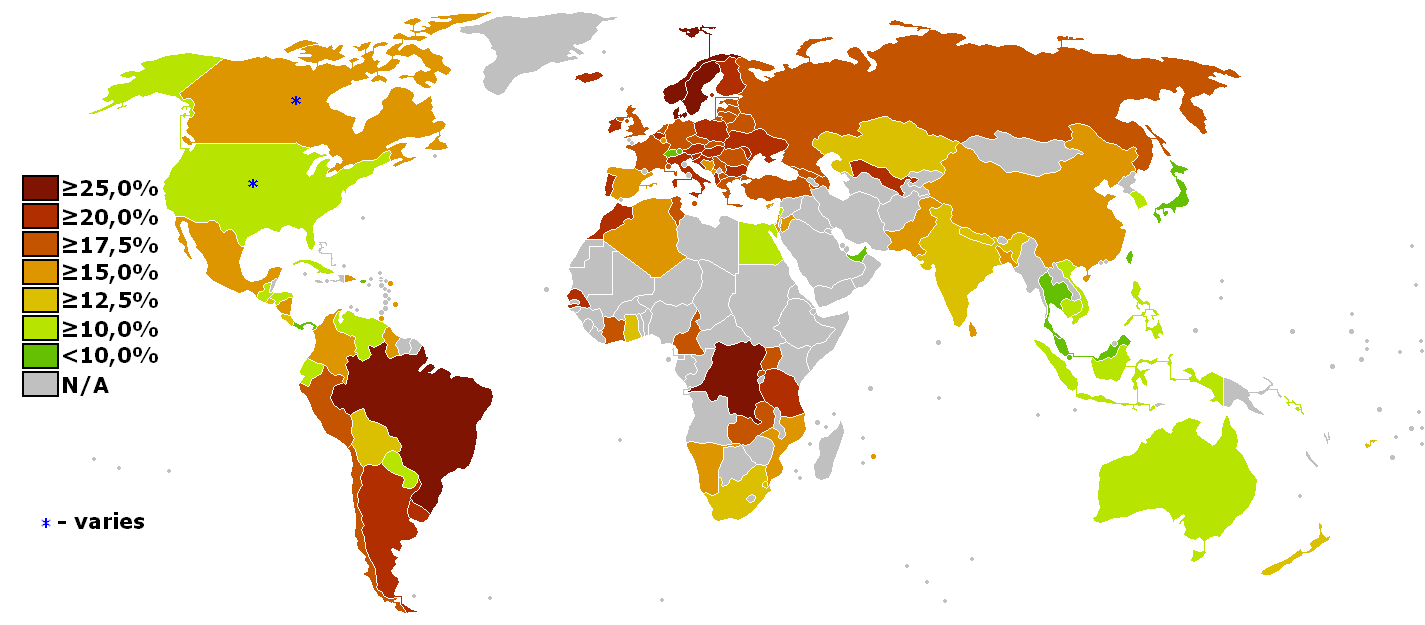

English: Tax rates around the world: VAT rate/G&S ...

English: Tax rates around the world: VAT rate/G&S ... 2011-01-04: 17 - 20

2011-01-04: 17 - 20 Pasty La Vista, Taxman: Victory as Chancellor cave...

Pasty La Vista, Taxman: Victory as Chancellor cave...Individuals or companies with an annual turnover over a certain value from taxable supplies, which currently stands at $58,000, needs to apply for VAT registration with HM Revenue & Customs as a 'taxable person', which can be an individual or partnership, company, club, association or charity. Once registered, a taxable person is charged VAT whenever a 'taxable supply' of goods or services is made. Companies supplying only VAT-exempt products cannot register for VAT whereas companies supplying zero-rated products have to apply as the supplies are VAT rated but at 0%. Once registered, you will be sent forms about 3 weeks before a tax period. A tax period is the length of time between VAT returns, which is usually a quarter. The VAT returns will need to be submitted within one month of the end of the tax period along with any VAT payable.