Pablo Este, owner of the South American steel company, Rosario Acero, SA, is currently trying to determine his company's optimal capital structure. Este must beside whether it should issue long-term debt in the form of bonds (notes + warrants) or long-term publicly traded stock (equity) through the company's first initial public offering (IPO). Management is seeking $7.5 million in capital in order to (1) pay down its working-capital line of credit, (2) repay long-term debt and (3) capital improvements, among other things.

Pablo Este's determination will arise from a variety of significant factors that play a role in the business. A quantitave analysis is provided first, then a FRICTO analysis is performed to determine whether the quantitative finding are consistent with what is best for the firm. Additionally, the Hamada equation will be used to un-leverage and re-leverage Rosario's beta based upon the new debt/equity ratios. Finally, a WACC will be calculated to fully examine the effects of each option of the firm's overall cost of capital.

English: Metropolitan Life Bldg., Manhattan, New Y...

English: Metropolitan Life Bldg., Manhattan, New Y... The Initial Public Offering (IPO) Prospectus for A...

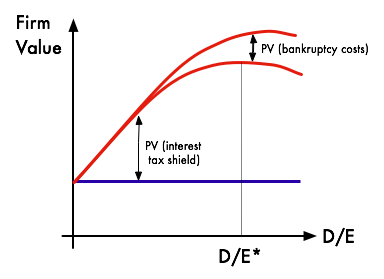

The Initial Public Offering (IPO) Prospectus for A... Trade Off theory diagram

Trade Off theory diagramEBIT/EPS Analysis

This analysis determines which method of capital financing will produce the higher EPS at a given level of EBIT. Central to this analysis is the determination of the EBIT*, the point at which both debt and equity financing would produce the same EPS. EBIT* is found by setting the EPS Debt equal to the EPS Equity, and solving for the corresponding EBIT. (See attachment 1). Based on the forecast Rosario Acero should use the debt financing option as every forecasted year produces an EBIT higher than EBIT*.

FRICTO Analysis

The FRICTO (Flexibility, Risk, Income, Control, Timing, and Other Concerns) analytical framework is used to fully examine the implications of Rosario's options to issue debt or equity.

Flexibility:

Debt: The issuance of debt to the private bondholders will reduce the firm's...

Attachments

No attachments were available for analysis, where are theY ????

3 out of 3 people found this comment useful.