The purpose of accounting is to provide financial information to management and the public. Generally accepted accounting principles (GAAP) are the minimum standards

and guidelines for financial accounting and reporting for state and local governments.

These principles were developed to establish requirements for the fair presentation and

comparability of financial information among governments. Adherence to GAAP ensures

that financial reports of all local governments will contain the same types and categories of funds and account groups and that the financial data will be based on the same

measurement and classification criteria.

A governmental accounting system should make it possible to (a) present fairly and with full disclosure the financial position and results of financial operations of the funds and account groups of the governmental entity in conformity with GAAP; and (b) determine and demonstrate compliance with finance-related legal and contractual provisions.

Several characteristics associated with government have influenced the development of governmental accounting principles and practices:

State law usually dictates the local government accounting policies and systems, may specify the type and frequency of financial statements, and usually defines the type and frequency of audits.

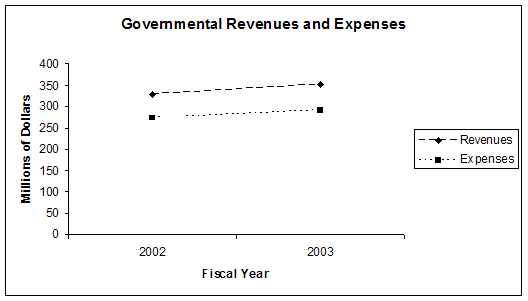

English: Seminole County, Florida Revenues and Exp...

English: Seminole County, Florida Revenues and Exp... English: The offices of the American Institute of ...

English: The offices of the American Institute of ... Wednesday 12 - Afternoon session

Wednesday 12 - Afternoon sessionGovernments have no powers in the proprietary sense. Accordingly, the measurement of earnings and the reporting of equity position is not a relevant accounting concept for governments.

Governments receive substantial financial inflows for both operating and capital purposes that are frequently subject to restrictions that prohibit or limit the use of the resources for other than the intended purpose.

A government's authority to raise and expend money is based on the adoption of a budget that, by law, must balance (the estimated revenues plus prior year's surpluses are sufficient to cover the projected expenditures).

The power to raise revenues and issue debt are restricted and generally defined by law.

Government accounting principles are not a...