Tax Efficiency:-

Tax efficiency has three aspects.

The first involves the administration and compliance costs of taxes. Tax efficiency is concerned with the convenience and certainty of a tax to the taxpayer, and with the cost of collection and compliance to the taxing unit. An efficient tax system would not impose excess cost to the taxpayer in the payment of the tax and would be collected and enforced at the lowest possible costs.

Administrative costs vary, of course, among individual taxes. Some types of taxes are more costly to administer than others. The cost of collecting and enforcing the federal income tax is large; yet these costs do not appear high, as a percent of revenue collected, although there is no real basis for making an objective determination. In regard to the compliance costs of taxes, they could be, rather high for certain taxes while appearing to be low enough to require little emphasis.

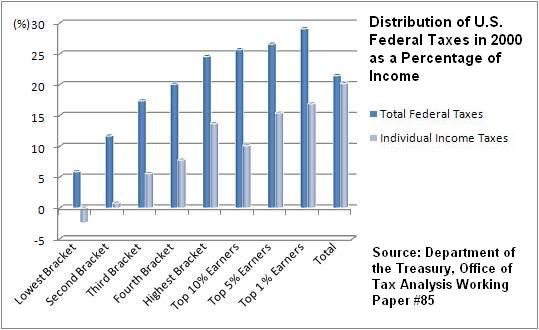

English: Further documentation of the data contain...

English: Further documentation of the data contain... Distribution of U.S. federal taxes for 2000 as a p...

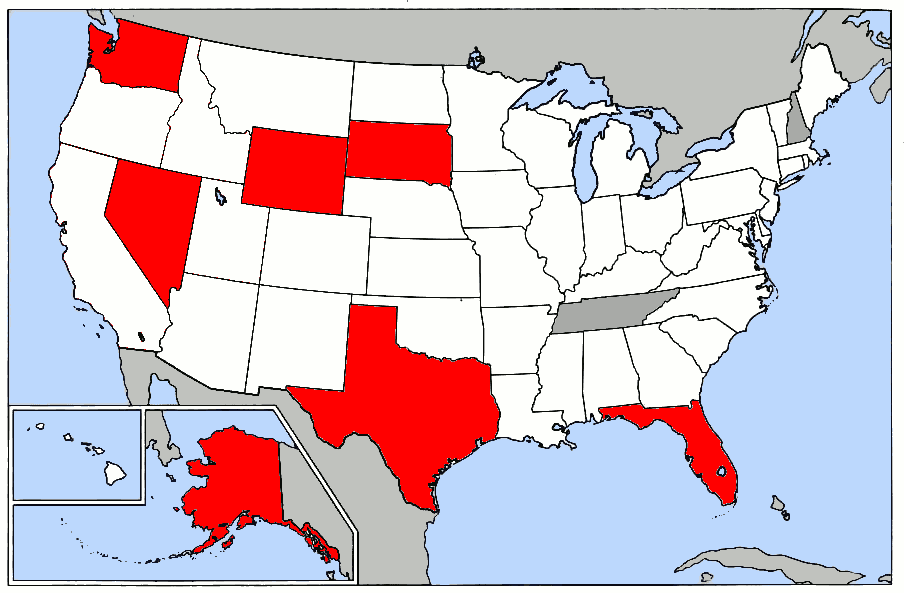

Distribution of U.S. federal taxes for 2000 as a p... Map of USA highlighting states with no income tax ...

Map of USA highlighting states with no income tax ...The second and third aspects of tax efficiency will be stressed instead, primarily because they involve the most important aspect of tax efficiency; namely the effects of taxes on the efficient operation of the economy.

The second aspect of tax efficiency involves an understanding of tax neutrality. Traditionally, economists view the economy as operating under a purely competitive framework. Given this framework, the allocation of resources in. the private economy would be optimal or at least efficient. As we have learned, the opportunity cost of increasing the size of the public sector is equal to the value of private goods and services sacrificed. But if, in addition to opportunity cost, private-decision-making in the market is interfered with and relative prices and individual behavior patterns are altered, taxes may cause an additional cost and have non-neutral and move the economy away from the most efficient use of...