IntroductionThe purpose of ABC is to address the first two questions at issue which deals with clarifying the cost structure of the Service Desk. The purpose of ITIL is to assist with the descriptions of the organizational functions and processes that occur within an IT Service Desk environment.

Traditional CostingTraditional cost systems are often associated with financial accounting focus and include direct materials, direct labour, and manufacturing overhead in their determination of product cost. For simplicity, we will assume here that overhead is allocated to individual products using a plant-wide overhead rate, although different companies may compute various departmental overhead rates. There is no causal relationship between the way in which overhead is allocated and the actual production process. Rather, overhead is allocated based on the number of units produced or the number of labour or machine hours used in production. (Hughes & Paulson, 2003 :23)Traditional cost accounting methods suffer from several defects that can result in distorted costs for decision making purposes.

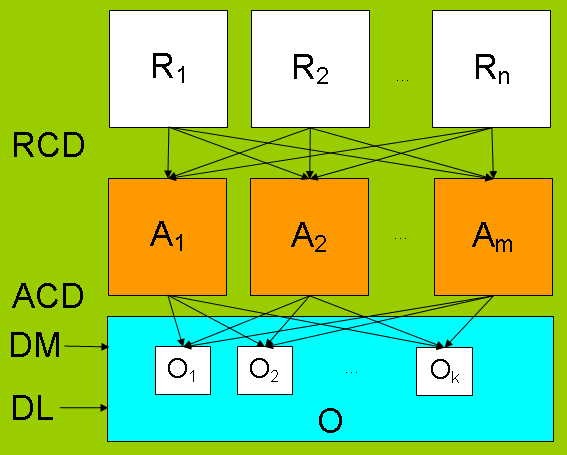

R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... Garrison, New York

Garrison, New York Secy of War Garrison & wife (LOC)

Secy of War Garrison & wife (LOC)(Garrison, Noreen & Brewer,2006: 339)All manufacturing costs -even those that are not caused by any specific product - are allocated to products. And nonmanufacturing costs that are caused by products are not assigned to products. Traditional methods also allocate the costs of idle capacity to products (Garrison, Noreen & Brewer,2006: 339).

Critics of traditional costing claim that this approach overcosts simple products produced in large batches and under costs more complex products produced in smaller batches. These cost issues result from the averaging nature of traditional cost system overhead allocation. (Hughes & Paulson, 2003 :23). The traditional system is easy and inexpensive to implement, but the information obtained could be too raw to be analyzed. ABC solves that problem but is expensive and time-consuming (Abdallah & Li, 2008: 12).

(Kaplin, Robert & Cooper, 1997: 83)Activity Based CostingActivity-based...