Introduction.

AMP has today flagged a possible $1.2 billion write down of its troubled offshore assets. The Chief Executive Andrew Mohl says AMP believes the carrying value of these assets is unlikely to recover for some time and it will therefore be prudent to reflect a more realistic view in the balance sheet. Therefore, he says the write- downs will largely be goodwill and not impact on the net assets of AMP's UK businesses. As the issue above, we make some definitions, analysis and comments.

1. Give a brief summary of the circumstances which give rise to goodwill.

a. Goodwill can only be recognized when an acquisition results in gaining control of an operation or entity. This term is defined and discussed in AASB 1013. As the AASB 1016, s 5.1 described, any difference between the cost of the investment in the associate and the investor's share of the net adjusted fair values is regarded as goodwill

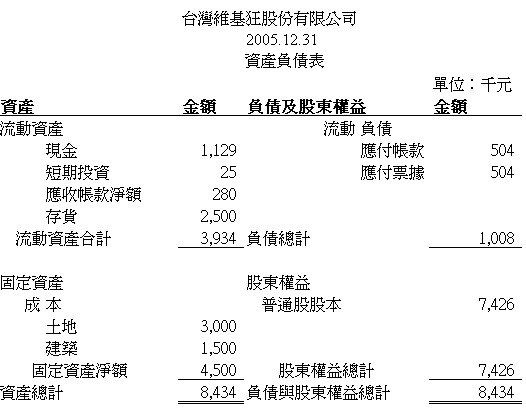

balance sheet in chinese

balance sheet in chinese Componenets of the asset side of the Federal Reser...

Componenets of the asset side of the Federal Reser... Entity up and running

Entity up and runningb. According to the AASB 1013, Section 4.1. Goodwill is internally generated by the entity must not be recognized by that entity. Goodwill, which is internally generated by an entity, is not permitted by this Standard to be recognized as an asset by that entity. This is principally because of the difficulty, or impossibility, of identifying the events or transactions which contribute to the overall goodwill of the entityÃÂì.ÃÂï Internally generated goodwill, which is not recognized as an asset will either go completely unrecognized or will be recognized as an expense.c. When an operation or an entity is acquired, we can recognize goodwill, which suggests that the particular assets and liabilities acquired must be capable of to be used together in meeting the objectives of the acquiring entity. This suggests that the operation or entity must be able to survive independently of...