Introduction

The efficient markets hypothesis (or EMH as it is known) and its predecessor, the random walk theory, are perhaps the most misunderstood concepts in the theory of investment. This is due partly to the back-to-front way in which the theory of efficient markets has evolved and partly to the misleading and emotive statements often ascribed to these theories, for example; 'Investment analysis is a total waste of time' and 'No one can beat the market'.

The question of whether the stock market is efficient in pricing shares and other securities has fascinated academics, investors, and businessmen for a long time. This is hardly surprising: even academics are attracted by the thought that by studying in this area they might be able to discover a stock market inefficiency which is sufficiently exploitable to make them rich, or at least, to make their name in the academic community.

Anyone investing on the stock market hopes to earn superior returns - to make a 'killing'.

Stock market of Brussels

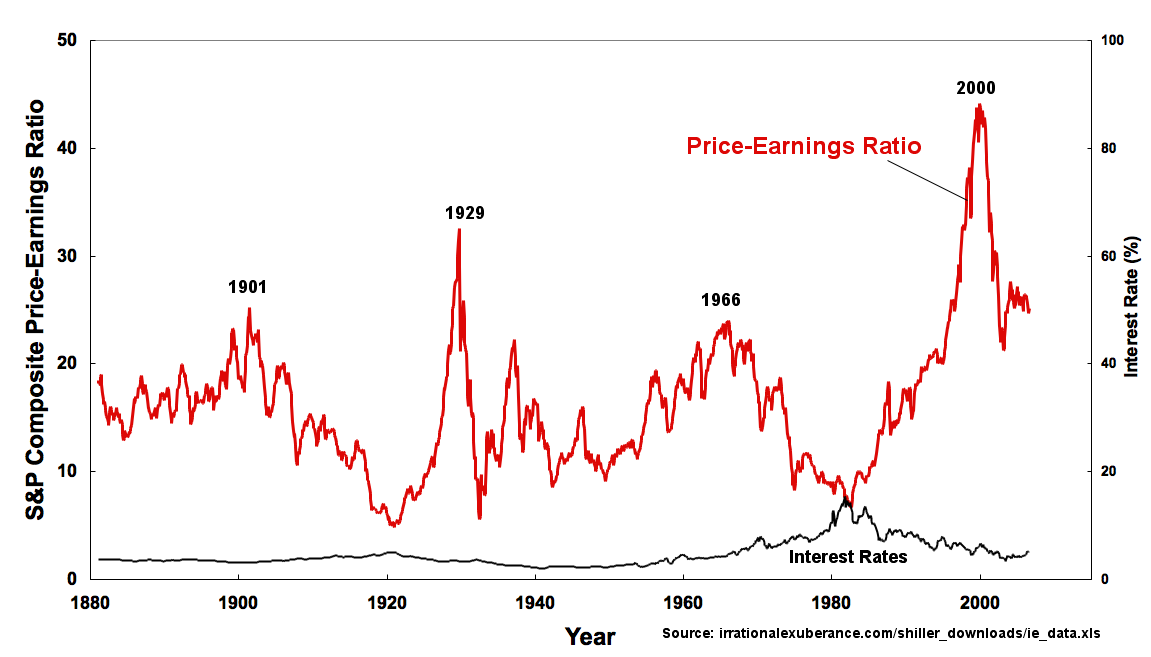

Stock market of Brussels Plot of S&P Composite Real Price-Earnings Ratio an...

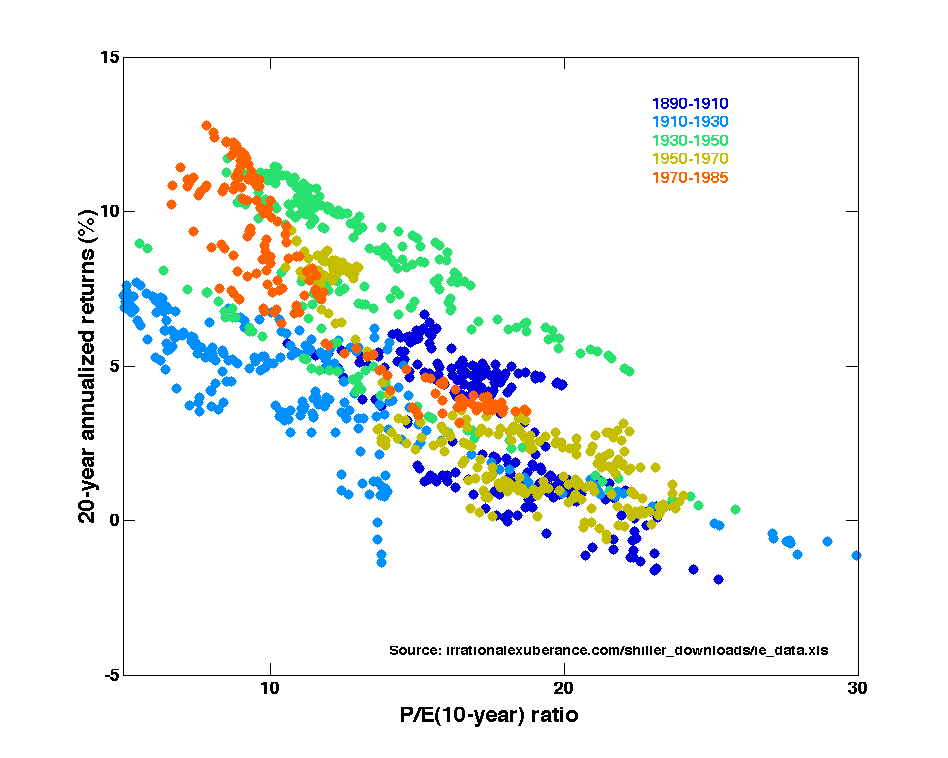

Plot of S&P Composite Real Price-Earnings Ratio an... Price-Earnings ratios as a predictor of twenty-yea...

Price-Earnings ratios as a predictor of twenty-yea...But making money from buying and selling securities on the capital markets is not, as many suppose, a matter of being able to predict the winners by studying the past. According to the EMH, such forecasts are nothing more than elaborate guess-work which, on average, are unlikely to be accurate. Ergo, in an efficient market undervalued or overvalued securities do not exist, and therefore it is not possible to develop trading rules which will 'beat the market'. However, if the market is inefficient it regularly prices securities incorrectly, allowing a perceptive investor to identify profitable trading opportunities. It is this that provides the fundamental reason for this paper.

The central hypothesis to this piece of work has been inspired by the principal theme of the EMH that 'no one can beat the market'. The general...