In the United States there are different types of entities that the public may require services from including business entities, governmental and not-for-profit entities. The foundation for these different types of entities is fundamentally different and therefore requires additional information in regards to accounting standards. Because the function of each of the different entities is unique to one another, the Financial Accounting Foundation (FAF) established the Governmental Accounting Standards Board (GASB) and Financial Accounting Standards Board (FASB) to develop General Accepted Accounting Principles (GAAP) for both governmental and governmental not-for-profit entities and businesses and nongovernmental not-for profit entities respectively.

The GASB is a private, non-governmental organization and its primary objective for is to establish GAAP for governmental entities, such as the Texas Office of the Attorney General as well as governmental entities that are classified as not-for-profit, such as the University of Texas. Distinguishably different, the FASB, which is also a private, not-for-profit organization, develops GAAP for businesses that are for-profit, such as Wal-Mart as well as not-for-profit organizations that are nongovernmental, such as the local Boys and Girls Club of Central Texas.

Wednesday 12 - Afternoon session

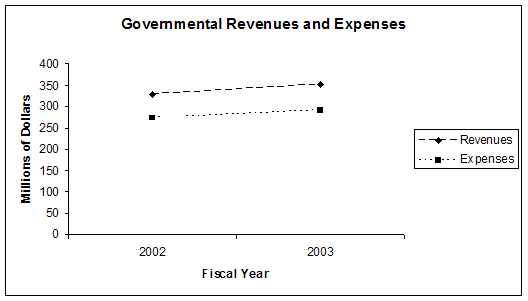

Wednesday 12 - Afternoon session English: Seminole County, Florida Revenues and Exp...

English: Seminole County, Florida Revenues and Exp... GaSb spiral growth

GaSb spiral growthBoth boards were established to improve financial accounting and reporting useful information in financial reports.

These two financial bodies are equivalent under the FAF in creating standards for financial accounting to respective entities. The FAF appoints each member of either board, GASB and FASB as well as supports the operating expenses for each. The FAF collects "contributions from business corporations; professional organizations of accountants, financial analysts, and other groups concerned with financial reporting." (Kattelus, 2002) Specifically for GASB, the FAF collects money from state local governments to help support the GASB operating expenses. Very important, the FAF keeps an arms distance with any one particular contributing entity in order maintain independent status for both GASB and FASB.