To:

Programming Department

From: Accounting Department

Date: 1/22/2006

Re: Depreciation Program Task

To Whom It May Concern:

I am writing in order to ask the Programming Department to design a program that will decrease the amount of time we use to calculate depreciation values. There are many other tasks that we must perform, and therefore, this would give us an incredible break in our work.

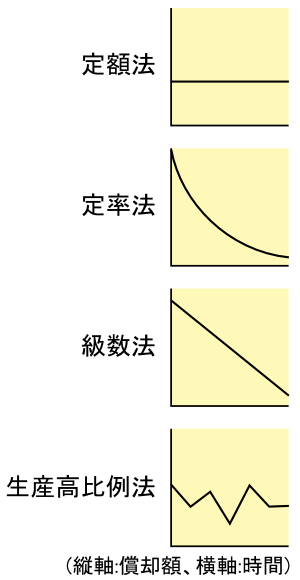

There are three types of depreciation that our company uses in order to evaluate the value of different accounts:

* Straight-line Depreciation: Charging an equal amount of depreciation expense for a plant asset in each year of useful life.

* Declining-balance Method of Depreciation: Multiplying the book value at the end of each fiscal period by a constant depreciation rate.

* Sum-of-the-years Digits Method of Depreciation: Using fractions based on the number of years of a plant asset's useful life.

The following pages display models and examples of how to complete the different forms of Depreciation.

English: Real estate economics - with depreciation

English: Real estate economics - with depreciation English: A graph of the depreciation of a 1993 Dod...

English: A graph of the depreciation of a 1993 Dod... 4 Depreciation methods (1:Straight-Line method, 2:...

4 Depreciation methods (1:Straight-Line method, 2:...Thank you for your help.

Thank you again,

Anthony Pittore

AP

Plant Asset: Computer

Depreciation Method: Straight-line Original Cost: $2,000.00

Estimated Salvage Value: $175.00

Estimated Useful Life: 5 years

Year Beginning Book Value Annual Depreciation Ending Book Value

1 $2,000.00 $365.00 $1,635.00

2 1,635.00 365.00 1,270.00

3 1,270.00 365.00 905.00

4 905.00 365.00 540.00

5 540.00 365.00 175.00

Total Depreciation ---- $1,825.00 ----

Example of Straight-line Depreciation:

Annual Depreciation Expense Calculation

Original cost

- Estimated Salvage Value

= Estimated Total Depreciation Expense

/ Years of Estimated Useful Life

= Annual Depreciation Expense $2,000.00

- 175.00

= 1,825.00

/ 5

= $365.00

Beginning Book Value

- Annual Depreciation

= Ending Book Value $2,000.00

- 365.00

= 1,635.00

Example of declining-balance method:

Plant Asset: Computer

Depreciation Method: Declining balance Original Cost: $2,000.00

Estimated salvage value: $175.00

Estimated useful...