Pricing * The cost can be broken up into following components: - Raw material cost (Water processing) - Labour charges - Packaging (Bottle, Label, cap & Carton) - Manufacturers margin - Excise duty - Sales tax - C & F agent/stockists commission - Retailer margin * There is considerable scope for varying these costs depending on technology, scale of operation of unit Pricing (Contd.) * Raw material and labour costs As discussed earlier there is considerable scope for cost reduction (a) by using minimum required processes/equipment (b) by employing casual labour Bisleri & Bailley : - Raw material Re 0.15 to 0.20 per litre of output - Labour Re 0.25 to 0.35 per litre Total Re 0.40 to 0.55 per litre ICE, Delhi spends Re 1.00 per litre of output Pricing (Contd.) - Packaging cost The package cost can vary depending on the choice of material (PET Vs. PVC), quality of cap, labels, shrink-wrap and Cartons A typical cost structure depending on PVC/PET usage and grammage of bottle is given below: Price (Rs.)

Composting facility, general view

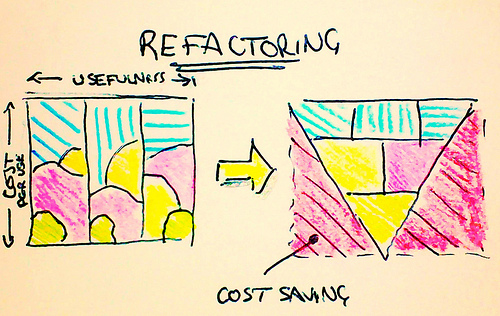

Composting facility, general view Growth multiplier/killer - Refactoring 2 - the epo...

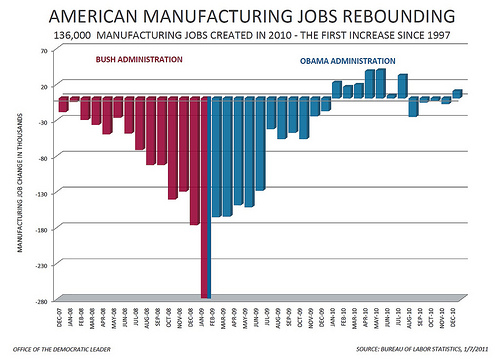

Growth multiplier/killer - Refactoring 2 - the epo... Manufacturing Jobs

Manufacturing JobsLow Medium High - Bottle 2.20 3.00 3.40 - Cap/shrink-wrap/label 0.35 0.50 0.50 - Carton (Rs 5-7.5 per pack of 12) 0.45 0.50 0.60 Total 3.00 4.00 4.50 Pricing (Contd.) - Total product cost + Manufacturers margin Low Medium High Process cost Re 0.40 Re 0.55 Re 1.00 Package cost Rs 3.00 Rs 4.00 Rs 4.50 ---------- ----------- ----------- Total cost Rs 3.40 Rs 4.55 Rs 5.50 Manufacturers margin Re 0.50 Rs 1.00 Rs 1.50 ---------- ----------- ----------- Ex factory cost Rs 3.90 Rs 5.55 Rs 7.00 Pricing (Contd.) * Tax structure Excise duty is charged in the following slabs: Rs 75 lakh + = 15% Rs 50-75 lakh = 10% < Rs 50 lakh = 5% Sales tax ranges from 7.7% and goes upto 10% for movement across states The small/medium players evade some of these taxes by under-invoicing A large investor can take advantage of backward area development and claim benefit (Mt. Everest Mineral Water enjoys a 5 year tax holiday) Pricing (Contd.) - Cost of taxation The Excise (assuming an average of 15%) and sales tax rate can be added to the final cost Low Medium High Ex factory cost Rs 3.90 Rs 5.55 Rs 7.00 Excise duty Re 0.60 Re 0.85 Re 1.05 Sales tax ~ Re 0.90 Re 0.90 Re 0.90 ---------- ----------- ----------- Product price Rs 5.40 Rs 7.30 Rs 8.95 Pricing (Contd.) * Cost of freight and Distribution This will vary as per the capability of manufacturer (In some cases, manufacturers deliver upto stockists location and in some cases delivery are made ex-factory). Also, the distances to carry will determine costs: Low Medium High Product price Rs 5.40 Rs 7.30 Rs 8.95 Freight & Distribution Re 0.30 Re 0.45 Re 0.65 ---------- ----------- ---------- Total Rs 5.70 Rs 7.75 Rs 9.60 Sale price Rs12.00 Rs12.00 Rs12.00 ---------- ----------- ---------- Trade margin Rs 6.30 Rs 4.25 Rs 2.40 Pricing (Contd.) Thus, a case of 12 will have the following price structure: Low Medium High* Cost of case Rs 68 Rs 93 Rs 115 Selling price Rs 144 Rs 144 Rs 144 Margin Rs 76 Rs 51 Rs 29 (52%) (35%) (20%) * Some manufacturers will price such bottles at Rs 14 thus selling at Rs 168 (a margin of Rs 53 or 32%) Pricing - Worst case scenario Since there is tremendous pressure on margins, a worst case scenario can be built from the point of view of a manufacturer: Selling price per 1 litre bottle = Rs 10 Retailer/distributor margin (Rs 40/case) = Rs 3.40 (-) Freight etc. = Rs 0.30 (-) --------- Product cost to trade = Rs 6.30 Excise (15%) = Rs 0.90 (-) Sales tax = Rs 0.80 (-) --------- Net product price for mfrs = Rs 4.60 Cost fo manufacturing Net realisation Low (Rs 3.40 per bottle) + Rs 1.20 per bottle Medium (Rs 4.55 per bottle) + Rs 0.05 per bottle High (Rs 5.50 per bottle) - Rs 1.10 per bottle Thus, ability to operate at low cost will be the key determinant of success unless the manufacturer is able to reduce the trade margin in his favour.

Investment & returns A plant of 40,000 lts/day is assumed to cost Rs 40 lakh or Rs 1 crore or Rs 5 crore and is expected to operate in 20, 40, 60, 80, 100% its rated capacity. Assuming a margin of Re 0.50 per litre sold, the ROI is as follows: ROI at Capacity utilisation (in %) Plant cost 20% 40% 60% 80% 100% Rs 40 lakhs 30 60 90 120 150 Rs 1 crore 12 24 36 48 60 Rs 5 crores 2.4 4.8 7.2 9.6 12.0 The low investment to high return indicates the proliferation of small operators even at 20% capacity utilisation. Whereas, the medium sized entrepreneur finds it just about OK at 25-30% capacity utilisation (which is normally the case and this explains the franchisee operations of Bisleri & Bailley). The high quality entrepreneur cannot survive until he reaches a capacity of 100% and that too can barely manage to survive

English: Sales tax labels on a record acquired in ...

English: Sales tax labels on a record acquired in ... English: "Sales Tax" ticket on the back of a Teddy...

English: "Sales Tax" ticket on the back of a Teddy... What I didn't make clear, and worth mentioning con...

What I didn't make clear, and worth mentioning con... Between Manufactures and Electricity Buildings

Between Manufactures and Electricity Buildings