F U N A C C O

CHAPTER 1

DEFINITION AND NATURE OF ACCOUNTING

Accounting - its function is to provide quantitative information, primarily financial in nature, about economic entities that is intended to be useful in making economic decisions.

Stakeholders - all parties who have interest in an entity, whether indirect or direct.

Stakeholders are grouped into two, namely:

External Users - groups or individuals who are not directly concerned with the day-to-day operations of the entity.

They make decisions that affect their relationship to the entity.

Internal Users - management personnel in all levels within an entity who are responsible for the planning and control of the operations and therefore, they have access to the day-to-day operations of the entity.

Some of the users of financial information:

Investors - concerned with the risk inherit in, and return provided by, their investments.

- need information to help them determine whether they should make additional, hold or sell their investments.

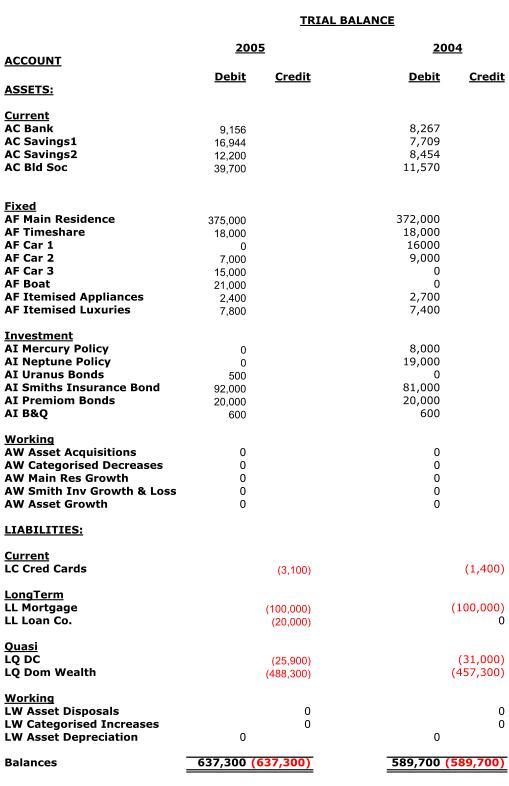

English: A sample Trial Balance from the example a...

English: A sample Trial Balance from the example a... General ledger accounts

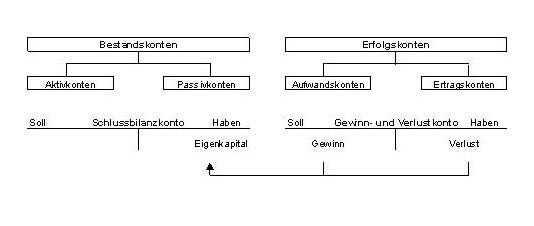

General ledger accounts English: Oracle General Ledger Accounting cycle

English: Oracle General Ledger Accounting cycleLenders - interested in information that enable them to determine whether their loans, and the interest attaching to them, will be paid when due.

Suppliers and other Trade Creditors - interested in information that enable them to determine whether amount owing to them will be paid when due.

Employees - interested in the information about the stability and profitability of their employers.

- interested in the information that will enable them to assess the ability of their employers to provide remuneration, retirement benefits and employment opportunities.

Customers - interested in the information about the continuance of an entity, especially when they have a long-term involvement with, or are dependent on, the entity.

Governments and their Agencies - interest in the allocation of resources and, therefore, the activities of entities.

Public - interested in information about the trends and recent developments...