Define the concept of scarcity: Scarcity: The goods available are too few to satisfy individuals' desires. Scarcity is a central concept in economics. Resources are scarce if any individual would prefer to have more of that good or service than they already have. Most goods and services are scarce - those that are not are known as free goods. Where goods are scarce it is necessary for society to make choices as to how they are allocated and used. Economists study (among other things) how societies perform the optimal allocation of these resources. For example, we may all want to own gold jewelry. However, the amount of gold available is limited, so it is necessary to make choices as to how it is allocated. In a market economy, this is achieved by trade. Individuals trade resources between themselves to reallocate resources to where they are most wanted. In a smoothly operating market system, the rate of exchange between different resources or price will adjust so that demand is equal to supply.

Wieser coined the terms marginal utility and oppor...

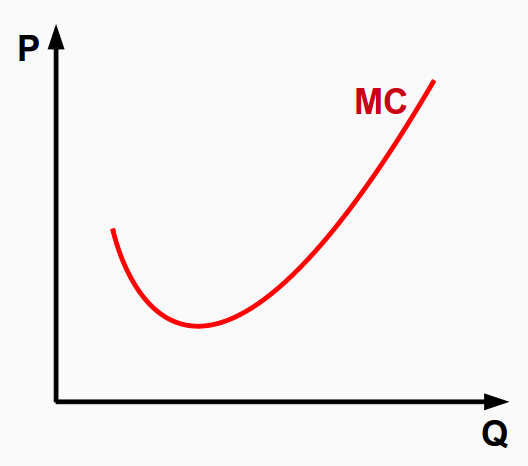

Wieser coined the terms marginal utility and oppor... English: marginal cost curve Polski: krzywa kosztu...

English: marginal cost curve Polski: krzywa kosztu... Typical progress of marginal cost

Typical progress of marginal costOne of the roles of the economist is to discover the relationship between demand and supply and develop mechanisms (such as pricing, incentives, or penalties) to achieve an optimal outcome (in terms of consumer welfare) between supply and demand. "Substantives" economists and economic anthropologists have argued that "scarcity" is a social construct and not a universal. Certain intangible goods are likely to remain scarce by definition or by design; examples include awards generated by honors systems, fame, and membership of elites. These things are said to have scarcity value; that is to say, all or most of their value is derived from their scarcity.

Define the concepts of marginal benefit / marginal cost. What is the relationship between marginal benefit / cost and scarcity? Marginal benefit is the benefit...