The relationship between law and standards

Companies act formed in 1900 - compulsory audit of the balance sheet - not the director.

Bigger business, role of directors determined by shareholders - appointing auditors, the requirement for a consistent approach.

1948 Companies act - balance sheet and profit loss account must give a true and fair view, disclosure levels introduced, audit requirements established. The accounting profession took on more responsibility. From 1948 because of SCANDALS (Pollypeck) - present, more and more principles, measurement and valuation rules, extended disclosure = true and fair override.

1985 and 1989 companies act changes in accounting practise

1) uniform formats

2) Publication requirements, what how to be published and when to recorded.

3) Accounting principles

4) Disclosure - amount of information disclosed is increased.

The ASB is a recognised body for the issuance of accounting standards that are to be complied with under the companies act.

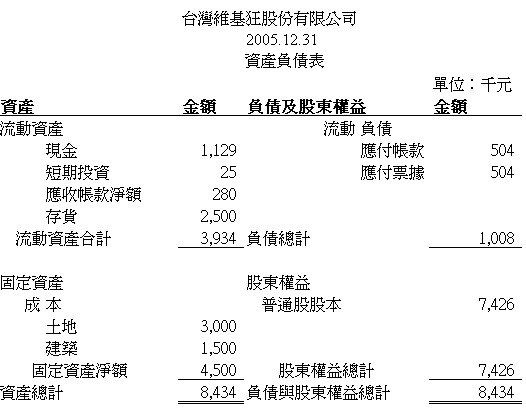

balance sheet in chinese

balance sheet in chinese English: Sample Domestic Balance Sheet (DBS)to be ...

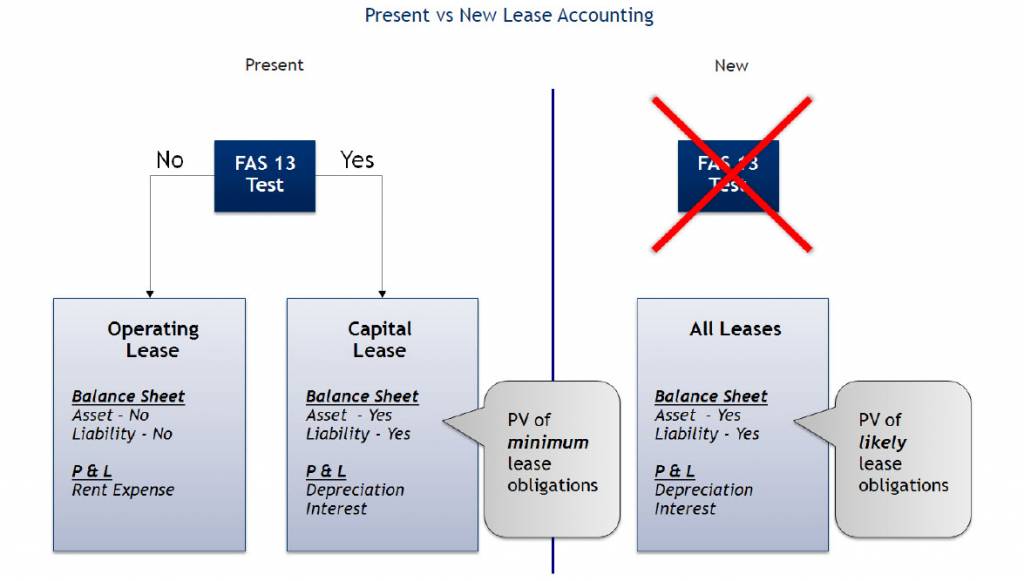

English: Sample Domestic Balance Sheet (DBS)to be ... English: Present vs. New Lease Accounting Standard...

English: Present vs. New Lease Accounting Standard...FRS and SSAPs adopted by the ASB are the Accounting Standards for the purposes of this act - standards need to be complied with but are not law.

Ardens - although standards aren't law. Giving a TFV is in the companies act. Generally, complying with standards gives a TFV, if not disclosure is required to justify departure from standards - the TFV override. Departures investigated by the FRRP and have the right to prosecute.

So what does the law require

1) give a TFV

2) Disclosure if TFV overridden

3) Auditor requirement to declare whether accounts have been prepared in accordance with standards

4) Standards are regulated - defective accounts can be prosecuted.

Aim - FRSs are developed within the context of current legislation with the aim of ensuring consistency between accounting standards and law

Coverage

Both law and standards cover measurement rules, disclosure and format items -

overlap = reinforcement

Amplify the law - SSAP 13; research and development; FRS 15; tangible fixed asset

Add to the requirements - FRS 1; cash flow statement not required under company law.

Overlap - problems with valuation and measurement

1) where accounting standards restrict law, accounting standards restrict the flexibility law offers; argument is that it increases consistency

lifo (SSAP 9) is not appropriate in the uk

exclusion of subsidiaries (FRS 2)

2) Restrictions of accounting standards

Government grants (SSAP 4)

3) the use of clever definitions in accounting standards preventing undesirable or creative accounting

extraordinary items (FRS 3)

quasi-subsidaries (FRS 5)

4) the use of the TFV override in standards to contradict law. ASB believes law allows too much scope for creative accounting => the use of clever words

investment property (SSAP 19)

goodwill amortisation (FRS 10)

TFV override in practise - research by Nobes and Parker

1) an increase in the use of the override

2) most often the companies act is overridden

3) common override

investment properties

omission of goodwill amortisation

consolidation - where companies have adopted merger accounting rather than acquisition accounting, even though by law should've been acquisition acounting

government grants

Problems with TFV - open to interpretations, changes over time. It is subjective and vague.

the true and fair view - recognition of economic substance rather than mere legal form - ruttermans

Alexander - TFV is all pervasive concept (type A)

Standards are a set of rules applied consistently applied to situations (type C)

In the uk type a = type c - balance between pronouncement and practise. Shifting further in the form of pronouncement

Essential purpose of TFV override - Nobes

1) to guide standard setters when developing type c rules

2) to enable auditors to depart from type c rules when necessary.

Risks of creative accounting, departing from the right TFV view - FRRP.

Bad

This really isn't an essay and there aren't many usefull facts

0 out of 0 people found this comment useful.