Based on the presented facts on the case, I have found:

ISSUIES:

(1) Whether the $6,500 of the award for covering the medical expenses and the $20,000 of the court award for punitive damages are includible in or excludible from the gross income of Ron Thompson.

(2) Whether Ron Thompson is entitled to include or exclude the medical expenses of $6,500 as itemized deduction in his federal tax return.

RULES:

1. Internal Revenue Code - ç104 Compensation for injuries or sickness.

2. Internal Revenue Code - ç 61(a).

3. Reg ç1.213-1 Medical, dental, etc., expenses. Final, Temporary & Proposed

Regulations.

4. Rev. Rul. 85-98, 1985-2 CB 51 -- IRC Sec(s). 104 Revenue Rulings (1954 - Present)

5. Rev. Rul. 76-144, 1976-1 CB 17 -- IRC Sec(s). 61 Revenue Rulings (1954 - Present)

6. Rev. Rul. 85-98, 1985-2 CB 51 -- IRC Sec(s). 104 Revenue Rulings (1954 - Present)

7. Rev.

AGI

AGI Expense Account

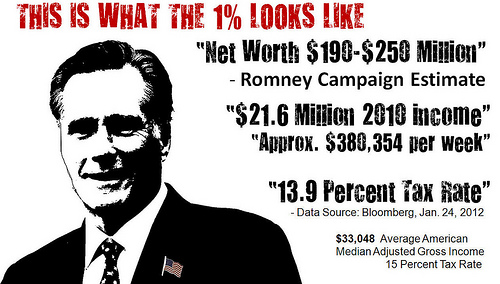

Expense Account Mitt Romney - The 1 Percent

Mitt Romney - The 1 PercentRul. 75-230, 1975-1 C.B. 93

ANALYSIS:

A taxpayer must include in gross income "all income from whatever source derived." I.R.C. ç 61(a). All realized accessions to wealth are presumed to be taxable unless the taxpayer can demonstrate that an accession fits into an exclusion provided by another provision of the Code.

One of these exclusions, found at section 104(a)(2), permits a taxpayer to exclude from gross income "the amount of any damages received on account of personal injuries or sickness." For exclusion purposes, the damages must be (a) based upon tort or tort-type rights, and (b) received on account of personal injuries or sickness. Commissioner v. Schleier, 515 U.S. 323, 115 S.Ct. 2159, 2167 (1995).

In Schleier, the Supreme Court, employing an example to illustrate whether certain recoveries were received on account of personal injuries or sickness, made it clear that the personal injury, whether physical or psychological, must be...