Accruals and Prepayments

What are accruals?

Accruals are those amounts of money which supposed to be paid by a certain period and are not yet paid.

Accruals are notes that do not enter in the trial balance.

Accruals are placed on the credit side of the balance sheet under the current liabilities in the case of expenses and on the debit side of the profit and loss, (if expense).

For Example:

Assume that water and electricity is paid at the end of every three months.

The bill was not paid on time. Details were

Amount water & Electricity bill duebill paid

LM 37531st March 200231st March 2002

LM 40030th June 20022nd July 2002

LM 35030th September 20024th October 2002

LM 40031st December 20025th January 2003

The water and electricity account appeared as:

Water & Electricity

2002

31st MarBank375

2nd JulyBank400

4th OctBank350

water and electricity paid on 5 January 2003 will appear in the books of the year 2003 as part of the double entry.

married put profit/loss graph

married put profit/loss graph English: Real estate economics - with depreciation

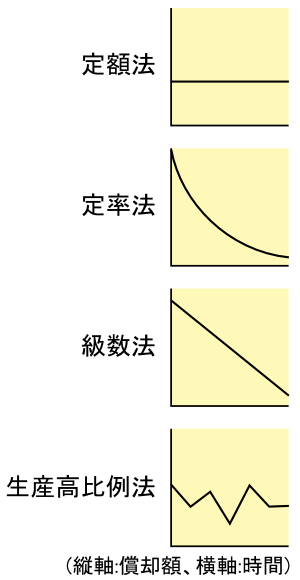

English: Real estate economics - with depreciation 4 Depreciation methods (1:Straight-Line method, 2:...

4 Depreciation methods (1:Straight-Line method, 2:...The total amount of water and electricity was of LM 1,525, which is needed to be transferred to the profit and loss account. But LM 1,525 was put on the credit side of the water and electricity account we would have LM 1,525 on the credit side of the account and only LM 1,125 on the debit side. To make the account balance the LM 400 water and electricity owing for 2002 but paid 2003, must be carried down to 2003 as a credit balance it is a liability on 31st December 2002. instead of water and electricity owing, this is called accrued or accrual.

The completed account can be shown:

Water & Electricity

20022002

31 MarBank375 31 DecProfit & Loss 1,525

2 JulyBank400

4 OctBank350

31DecAccrued C/d400

15251,525

2003

1st JanAccrued b/d 400...