Accy 202

'The view that accounting standard setters consider the economic, political and social consequences of accounting standards is consistent with the view that accounting reports, if compiled in accordance with accounting standards and other generally accepted principles, will be neutral and objective'

SYNOPSIS

Objectivity and neutrality are the ultimate goals of general purpose financial reporting. However there are many factors involved that make this goal almost impossible to attain. Economic, political and social issues are huge influences on the Accounting Standard setting process, and these influences spill over into everyday accounting, with personal gain often ahead of reliability and objectivity. Users of financial reports have demands that need to be satisfied, and regulatory boards involved in Standard setting have done their best to ensure that information is clear and reliable. Considering these factors, Accounting does not exist in a vacuum, Accountants are human beings, not robots and the profession has strict guidelines and heavy penalties for unprofessional or fraudulent activity.

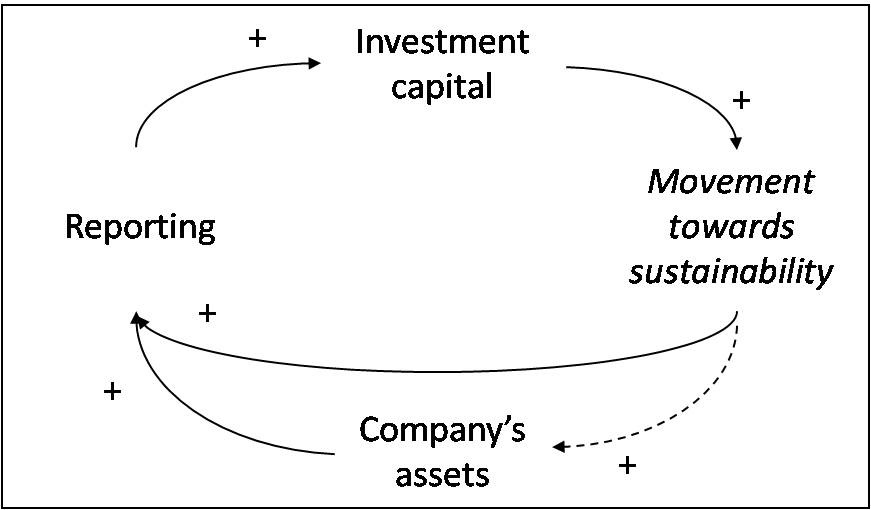

English: By incorporating sustainability investmen...

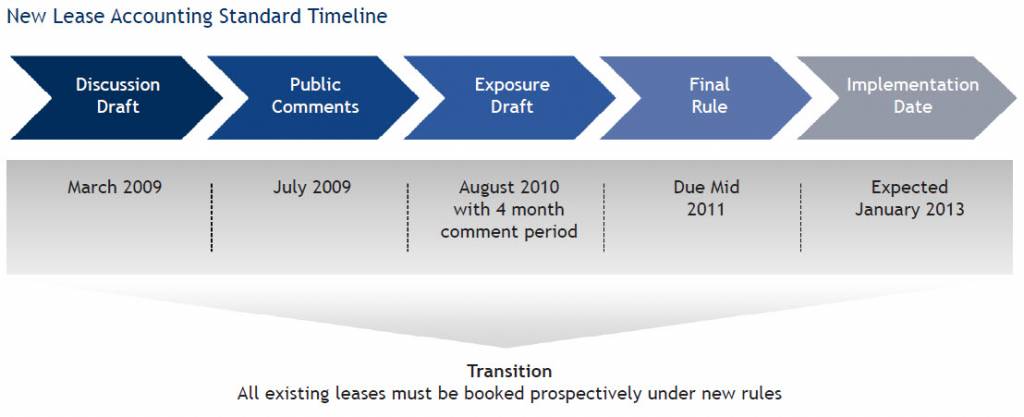

English: By incorporating sustainability investmen... English: New lease accounting standard timeline

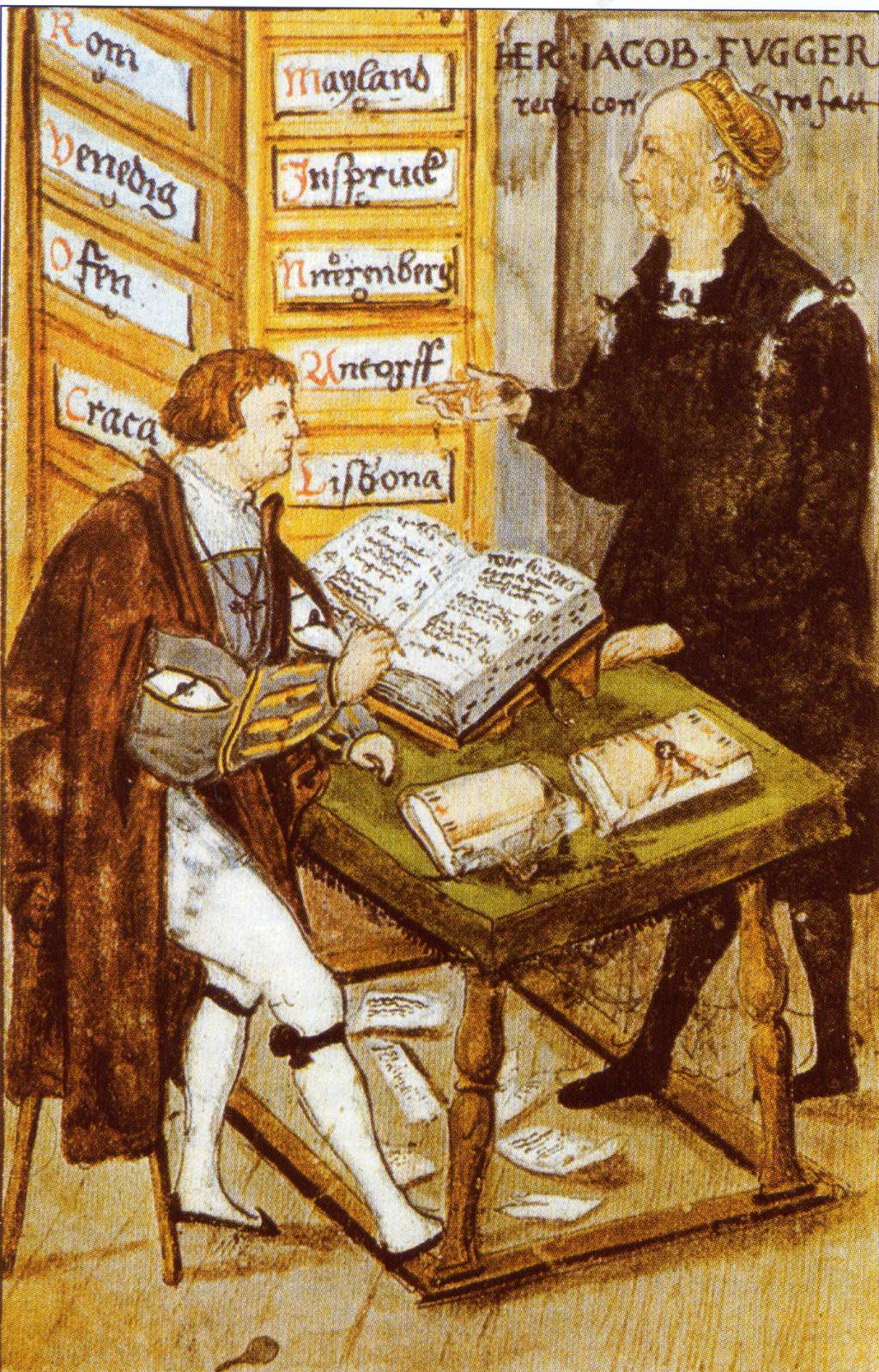

English: New lease accounting standard timeline office of Jacob Fugger; with his main-accountancy ...

office of Jacob Fugger; with his main-accountancy ...It is thus clear that every attempt is made to acknowledge the operating societal factors, gauge the impact they have on different industries at different times and move from that point. The result than, has to be, the best attempt at a neutral and objective report by the professional accountant.

Economic, political and social issues are powerful driving forces within any society. These issues therefore need to be focused on when major decisions in industries, are being made. One industry that heavily relies on, and incorporates economic, political and social issues in its' decision-making, is that of Accounting. The Accounting profession is made up of many standards and regulatory boards that govern the way in which entities maintain their general-purpose financial reports.

Accounting standards set minimum benchmarks of the quality required in financial reporting. They specify that reporting entities...

Not very interesting but nice info

this had a lot of information that i needed, even if it was not interesting t read.

9 out of 9 people found this comment useful.