Current and Non-Current Assets Paper

name

ACC/400: Accounting for Decision Making

May 10, 2010

instructor

�

Current and Non-Current Assets Paper

Assets are "resources owned by a business" (Kimmel, Weygandt & Kieso, 2007, p. 10) which are expected "to increase the value of a firm or benefit the firms operations" (Investopedia, 2010, para. 3). Assets are necessary because they are used to fund operations and expenses of a business. Assets are divided into two categories, current and non-current, which will be compared and contrasted in the paper. Also discussed in the paper will be the order of liquidity and how the order of liquidity applies to the balance sheet.

Compare

Assets hold value for a company and can be converted to cash or used up by a company.

Assets are classified into two categories, current and non-current. Classifying assets is helpful because it helps determine if the company has enough assets to pay its debts when they come due (Kimmel, Weygandt & Kieso, 2007).

SOMF Asset Patterns

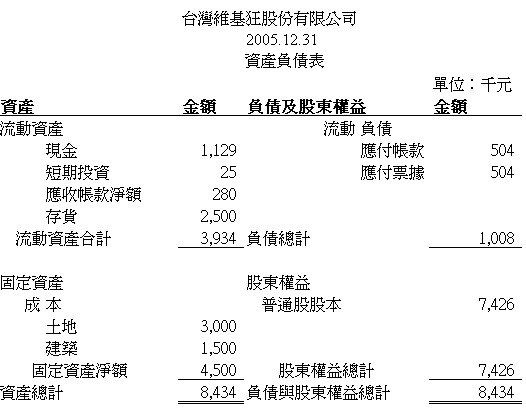

SOMF Asset Patterns balance sheet in chinese

balance sheet in chinese English: Navy and Coast Guard officers and chiefs ...

English: Navy and Coast Guard officers and chiefs ...Current Assets

Current assets are "assets that a company expects to convert to cash or use up within one year" (Kimmel, Weygandt & Kieso, 2007, p. 49). Current assets are also referred to as short-term assets. Examples of current assets are: cash, accounts receivable, notes receivables, marketable securities, prepaid assets, and other liquid assets that can be readily converted to cash (Investopedia, 2010).

Non-Current Assets

Non-current assets are assets that will not be converted to cash or used up within one year. Non-current assets are also referred to as long-term assets. Examples of non-current assets are: leasehold improvements, long-term investments, long-term notes receivable, intangible assets, and fixed assets such as property, plant and equipment (Simple Studies, 2010).

Contrast

The difference between current assets and non-current assets is the time in which the asset will be converted...