Faces to the competitive business environment, many manufacturing and service organizations operate have already significantly changed in the past 30 years. These new changes have rendered traditional cost accounting methods lack of managers' demands for correct, detailed, correlative information for decision making such as strategic thinking, production promotion plan and cost control etc.. Also the new modern methods have effectively reduced the correlative importance of direct labor cost as production costing. As a result, management accounting is trying to use more logical and efficient way to admeasure costs in the new fields.

According to Larry Sawyer said, the tenth commandment of accounting is "to know new methods" (Lawrence B. Sawyer 1983). Activity-based costing (hereinafter, ABC) systems is clearly a modern method which is increasingly being used in management accounting place. The rising trend of ABC systems using can be reduced in part to consumers' high quality products wants and increasing international business competitions.

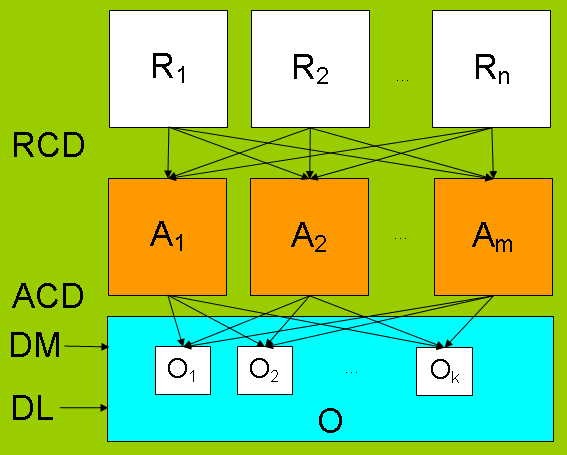

English: Simprocess integrates Process mapping, de...

English: Simprocess integrates Process mapping, de... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver...(For instance in China)

Since the manager who examine and evaluate the costing of product and the scope of management accounting includes" reviewing the reliability and integrity of financial and operating information . . . and appraising the economy and efficiency with which resources are employed," (Altamonte Springs 1978) managers need a thorough understanding of activity-based costing.

Traditional costing systems usually utilize a single basis, (e.g. direct labor) to distribute the indirect costs to all products and services.Deborah W. Tanju 1991 The manufacturing overhead costs have been subjectively admeasured to products based on direct labor hours, ignore whether or not a cause and effect relationship existed between direct labor hours used and the reasons of overhead costs.

According to Robert Kaplan, (Robert S. Kaplan 1990) the final goal is to develop a completely integrated cost system with high data quality and linked databases. The system...