With the Nation in recession, lower interest rates provoke the American population to buy and refinance homes across the country. On the other hand, there may be more mortgage payment default (foreclosures) due to the economic misfortune some people encounter. Much attention has been turned to the housing domain.

Over 67% of Americans own their homes. Housing has always been an important sector in the US economy. In 2000, the housing sector as a whole contributed $1.2 trillion to the Gross Domestic Product, or 12.1% of the U.S. economy. Home ownership creates jobs and national wealth not only at the moment a house is built, but also through the time the house is placed on the market, to the time the new owner furnishes and remodels it following the purchase. In 2000, housing construction generated 3.5 million full-time jobs, $113.8 billion in wages and salaries, and $60.9 billion in federal, state and local tax revenues and fees in the US.

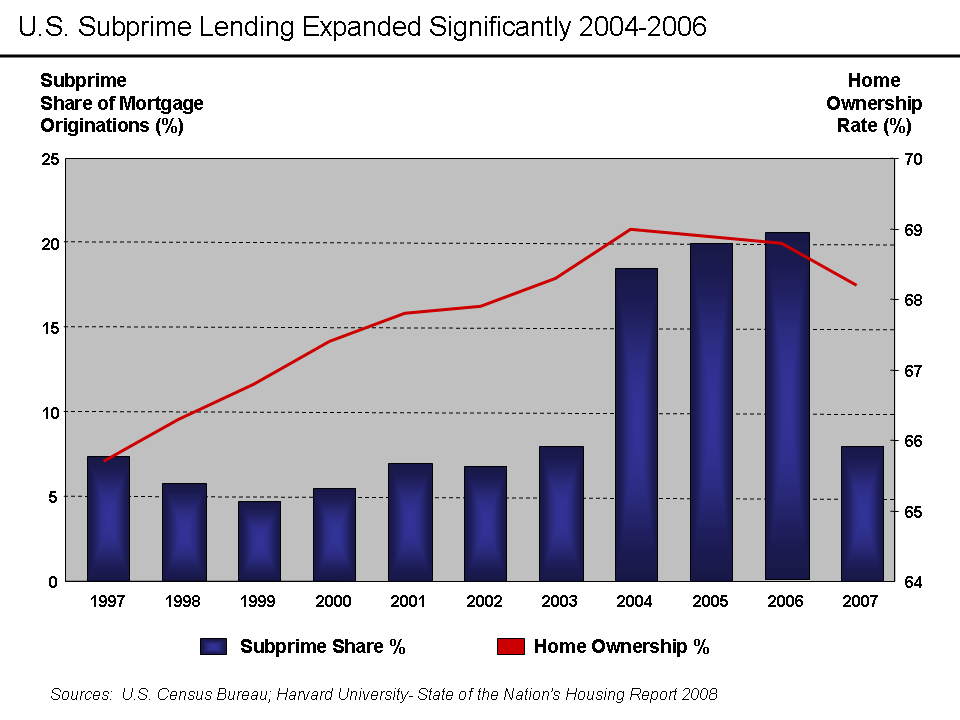

U.S. Subprime lending expanded dramatically 2004-2...

U.S. Subprime lending expanded dramatically 2004-2... English: The Colonial Revival headquarters of Fann...

English: The Colonial Revival headquarters of Fann... 20090110 money printing-01

20090110 money printing-01In 2000, owners of newly built single-family homes spent an additional $5.9 billion on furnishing, decorating and improving their houses in the U.S. (Amita Shah, Pg. 10)

Buying a house is the largest purchase and investment in most Americans lives. And for most people, buying a house behooves them to get a mortgage to finance the purchase. The mortgage rate moves together with the long-term bond rates. The interest rate an individual borrower gets also depends on the borrower's credit record, income, the ratio of loan amount to the value of the house, etc. How the United States' housing finance system works is not as lucid as most think, it is a system that involves a lot of different financial institutions and financial instruments that help route investors' funds into the purchase market and obtain additional funds for mortgage lending.