Break-even analysis is a management tool which supports planning and decision making by clarifying the effects of change in output and selling price on profitability. It illustrates the relationship between output, sales revenue, variable and fixed costs and profit. A business breaks even when contribution (sales - variable costs = contribution) equals fixed costs, meaning all costs are covered, neither a profit nor loss is being made. A company can use the break-even analysis also for calculating a pre-determined profit/turnover or for the decision whether to accept an additional order or not.

Usually the break-even point is calculated by dividing fixed costs by contribution getting break even units. A company that produces a multi-product mix has not only one contribution but several for each product. It can not calculate break even units but it could use the profit volume ratio by adding up all separate contributions and dividing the result by total sales.

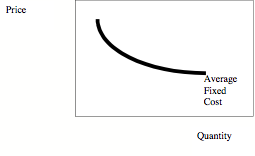

Average Fixed Costs

Average Fixed Costs Smile Pinki, Smile Train

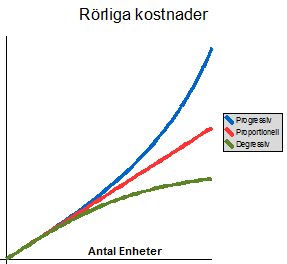

Smile Pinki, Smile Train English: Variable costs in swedish Svenska: Rörli...

English: Variable costs in swedish Svenska: Rörli...The fixed costs are then divided by the previously calculated profit volume ratio. Thereby a firm gets the turnover which is necessary to break-even. For the sake of completeness, a company can also use average variable cost and sales turnover to calculate contribution for a multi product mix.

Underlying this concept of break-even analysis are some basic assumptions:

It assumes that, if a range of products is sold, sales will be in accordance with a consistent sales mix over a period. That assumption is risky, because a constant sales mix is not likely to hold throughout the period. The second assumption is that costs can be accurately classified in variable and fixed costs using for instance the Hi-Lo method, but therefore the relationship between variable and fixed costs must be consistent between the extremes. That can be proofed as to be false in same cases (e.g.