Simply stated, the financial accountant is the number cruncher while the managerial accountant is the analyzer. However, it is not that simple. Most experts are fairly consistent with their definitions of what the financial accounting entails, however, defining managerial accounting appears to be opinion dependent. As the population of the occupation grows so does the defined responsibilities involved.

The general consensus of financial accounting is that it reports past results using historical-cost accounting. Financial accounting is backward-looking and sacrifices decision relevancy for objectivity (Bromwich, 1988, p. 26). According to Answers.com accounting is defined as "the bookkeeping methods involved in making a financial record of business transactions and in the preparation of statements concerning the assets, liabilities, and operating results of a business. When I envision an accountant I cannot help but see the squirrelly little FBI CPA in "the Untouchables", the one that took down Capone on tax evasion. I see stereotyped, the short, bawling guy with the genius IQ, in glasses, "crunching" numbers in the adding machine.

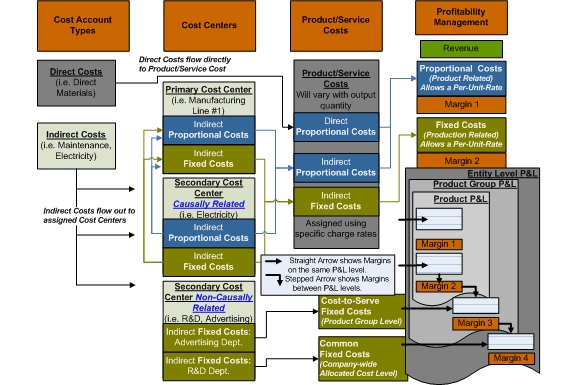

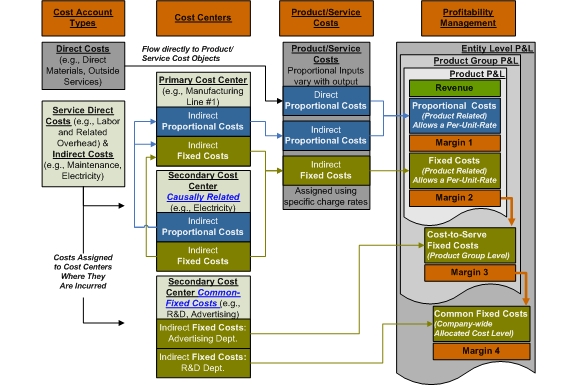

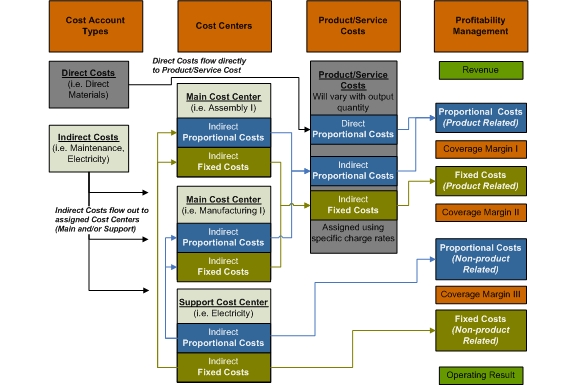

English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr... English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr... English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr...The Financial accountant or CFO is the head of the finance department that runs all the reports, puts all the numbers in, takes care of the assets, liabilities, payroll, and taxes. The managerial accountant goes one step beyond by using the historical data compiled to make decisions for the present and future direction of the company. Managerial accountants are becoming more and more beneficial to companies and their future.

Managerial Accounting 3Managerial accountants have many definitions, with several very constant characteristics. Professor Michael Bromwich (1988) states that management accounting is "future-oriented, is dynamic, produces forward looking figures and is meant to be decision and control relevant, should not be too concerned with objectivity and is not generally subject to external regulations" (p. 26).

In a message from the chair, Larry White (2005)...