Questions 2-4

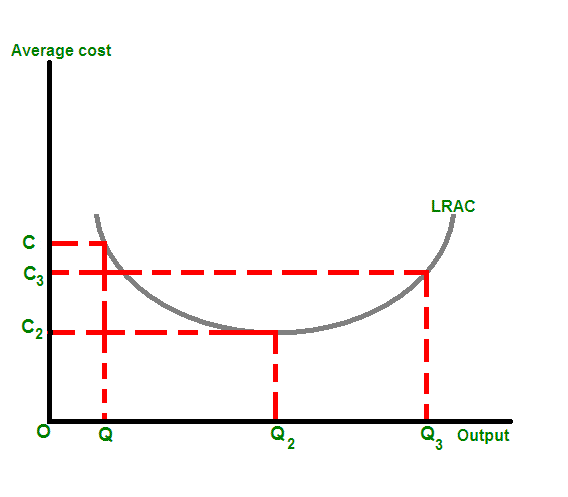

The diagram shows that as more is produced, and so...

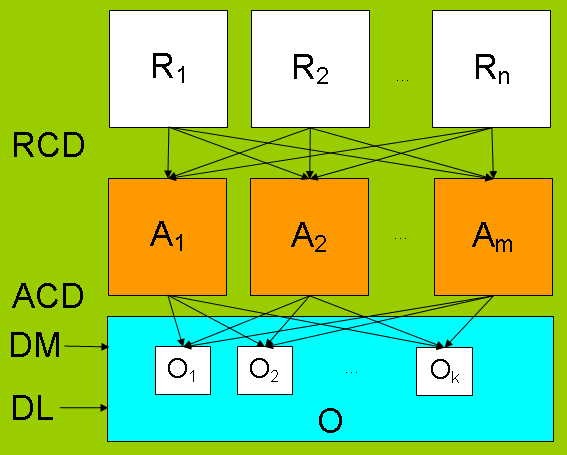

The diagram shows that as more is produced, and so... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver...The estimated costs calculated using the activity-based costing method is very different from the existing standard unit costs and the revised unit costs. Exhibit 3 uses the traditional cost allocation system, which allocates all costs based on measures of volume. In the standard unit costs, Destin Brass uses direct labor as the only cost driver, which rarely meets the cause-effect standard wanted in cost allocation. Exhibit 4 is similar to exhibit 3, but instead, 4 uses materials and machine hours as the cost driver instead of just direct labor. The new costs are calculated by using the ABC system, which allocates costs that are caused by non-volume-based cost drivers. After recognizing the overhead activities, costs of overhead resources used for the activities are allocated to the activities using cost drivers. Then pooled costs of each activity are allocated to products, using the cost drivers. It takes one large overhead cost pool and breaks it down into several pools, which for this company are: receiving and materials handling, machine usage and maintenance, packing and shipping, and engineering. These have a cause-effect relationship with activities and resources that are used. So unlike exhibit 3 and 4, the new system breaks down the overhead costs a lot more. The new estimated costs are more accurate because the amount allocated to each of the overhead activities for each product is more detailed. It shows the percentage of how much each activity is performed on each product.

All 3 products' unit costs in the new system are different from exhibit 3 and 4. Unit price for valves has a slight change compare to the standard unit price, but for pumps and flow controllers, there is a dramatic change.

Destin Brass are well under their 35% gross margin goal for...