There are two broad categories in accounting, financial accounting and managerial accounting. They differ in the type of user of the information presented. Financial accounting is concerned with preparing financial statements for external decision makers, such as stockholders and creditors. Managerial accounting presents information for internal decision making my managers.

Financial accounting involves record keeping. A major objective is the preparation of financial statements. These statements include the balance sheet, statement of cash flows, income statement, and change in owner's equity (Introduction to financial accounts, 2005). This information will help external users decide if they should invest in the company, lend money to the business, or the profits which the company must pay tax on.

Managerial accounting uses much of the same information as financial accounting, but can be tailored to fit the specific needs of the manager at a given time. Financial accounts are prepared for a given period, usually one year, while management accounts can be prepared for any period.

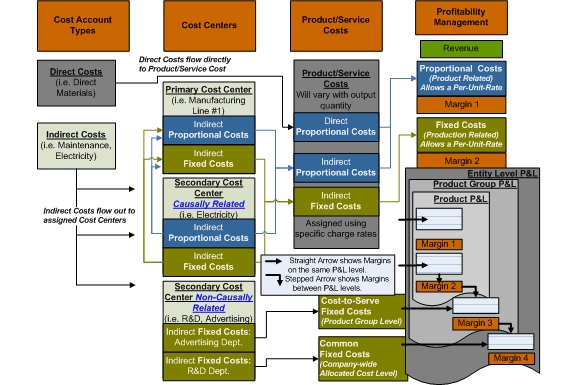

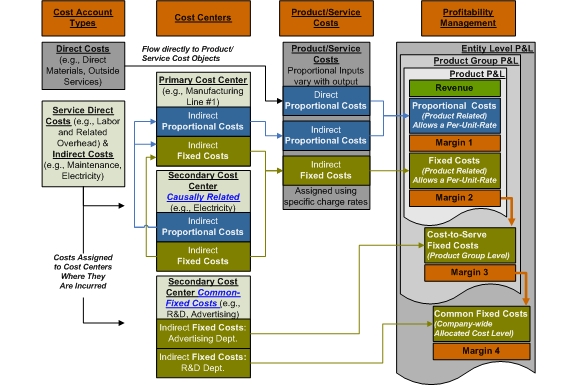

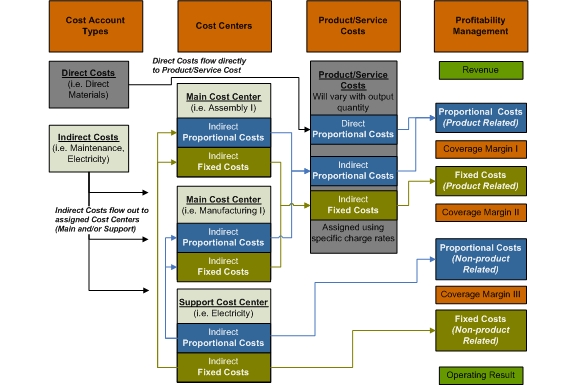

English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr... English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr... English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr...For example, retail businesses often prepare daily reports on sales and stock levels (Comparison of financial and management accounting, 2005). Managerial accounting involves more than just financial statements. Managerial accounting can include cash flow analysis, break even analysis, budgeting, and financial ratio analysis. Management accounting can be used to plan for the future by understanding how economic events affect the business (Bromwich, 1988). Managers can evaluate the state of the business by looking at efficiency, and analyzing costs.

There are several ratios which are useful to managers. Liquid ratios measure the company's ability to meet obligations using available assets. Solvency ratios measure the extent to which a company is financed by debt. Activity ratios measure the company's use of resources. Profitability ratios measure management's effectiveness (Managerial Accounting, 2005).

The Institute of Management Accountants Standards of Ethical...