Profit and Loss Account

In most businesses profit is the driving force behind the decision process. The amount of profit made by the firm is often an indicator of performance. The level of profit is measured / calculated through the profit - loss account.

The profit and loss account illustrates all the business transactions over the time period (usually one year).

The profit - loss account is divided into 3 sections. These sections are combined to create the final account. The sections are;

Trading account

Profit and loss account

The profit and loss appropriation account

The Trading Account

The trading account highlights the revenue earned from selling products (turnover) and the cost of these sales. This section allows you to calculate GROSS PROFIT

Gross Profit = turnover - cost of sales

Profit and loss account

After calculating gross profit, the profit and loss account will allow you to calculate information upto and including PROFIT ON ORDINARY ACTIVITIES BEFORE TAX.

married put profit/loss graph

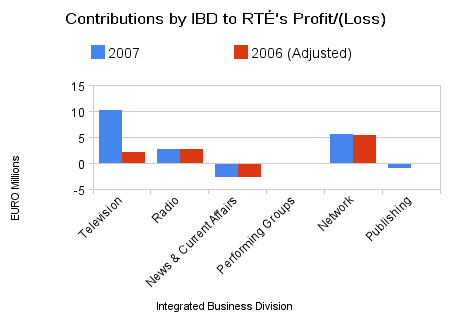

married put profit/loss graph Contributions by ibd to rté's profit (loss)

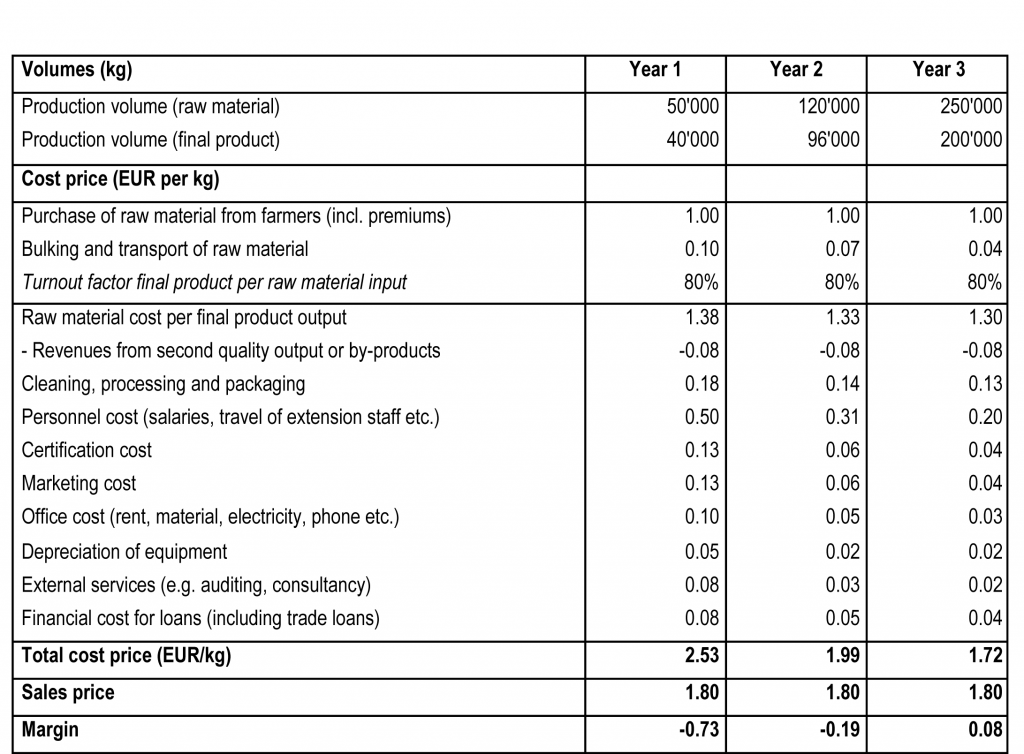

Contributions by ibd to rté's profit (loss) English: Table 4: Example of a profit and loss cal...

English: Table 4: Example of a profit and loss cal...This includes;

OPERATING PROFIT (NET PROFIT) = Gross profit - expenses

PROFIT ON ORDINARY ACTIVITIES BEFORE TAX = Operating Profit + non-operating income - interest payable

The Profit and loss appropriation account

This section highlights how the company's profit or loss is distributed. This section highlights the PROFIT AFTER TAX and the RETAINED PROFIT CARRIED FORWARD.

PROFIT AFTER TAX = profit on ordinary activities before tax - corporation tax

RETAINED PROFIT CARRIED FORWARD = profit after tax - dividends

Profit and Loss Account

This page tells you all about what a profit & loss account is and how it is constructed. The profit and loss account differs significantly from the balance sheet in that it is a record of the firm's trading activities over a period of time whereas the balance sheet is the financial position at a moment in time.

Not an essay

I don't See where it says that notes are an acceptable substitutefor actually writing something coherent.

0 out of 0 people found this comment useful.