There are five steps in the accounting cycle, which when finished lead to the trial balance, adjusting entries, preparation of the financial reports and the closing entries. These steps are repeated during each accounting period, monthly, quarterly or yearly. I work for Fidelity Investments and the accounting cycle from start to finish is electronic. This helps the accountants, as they will always have a paper trail that is important, especially when it is time to meet with the auditors. This "paperless environment" is one of the first and has been upgraded from the corporations own system to the utilization of Oracle. There five steps of the accounting cycle are identify, prepare, analyze, record and post. Once these steps are accomplished, the financial statements and closing of accounts can be done.

An item may be purchased two ways. The first is for the employee to call and order it. The second is to fill out a requisition form via the E-uest system.

English: Oracle General Ledger Accounting cycle

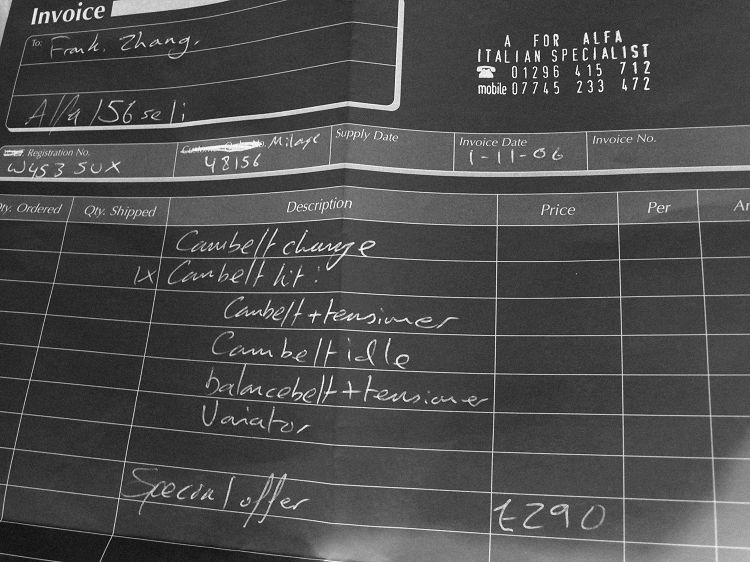

English: Oracle General Ledger Accounting cycle Invoice

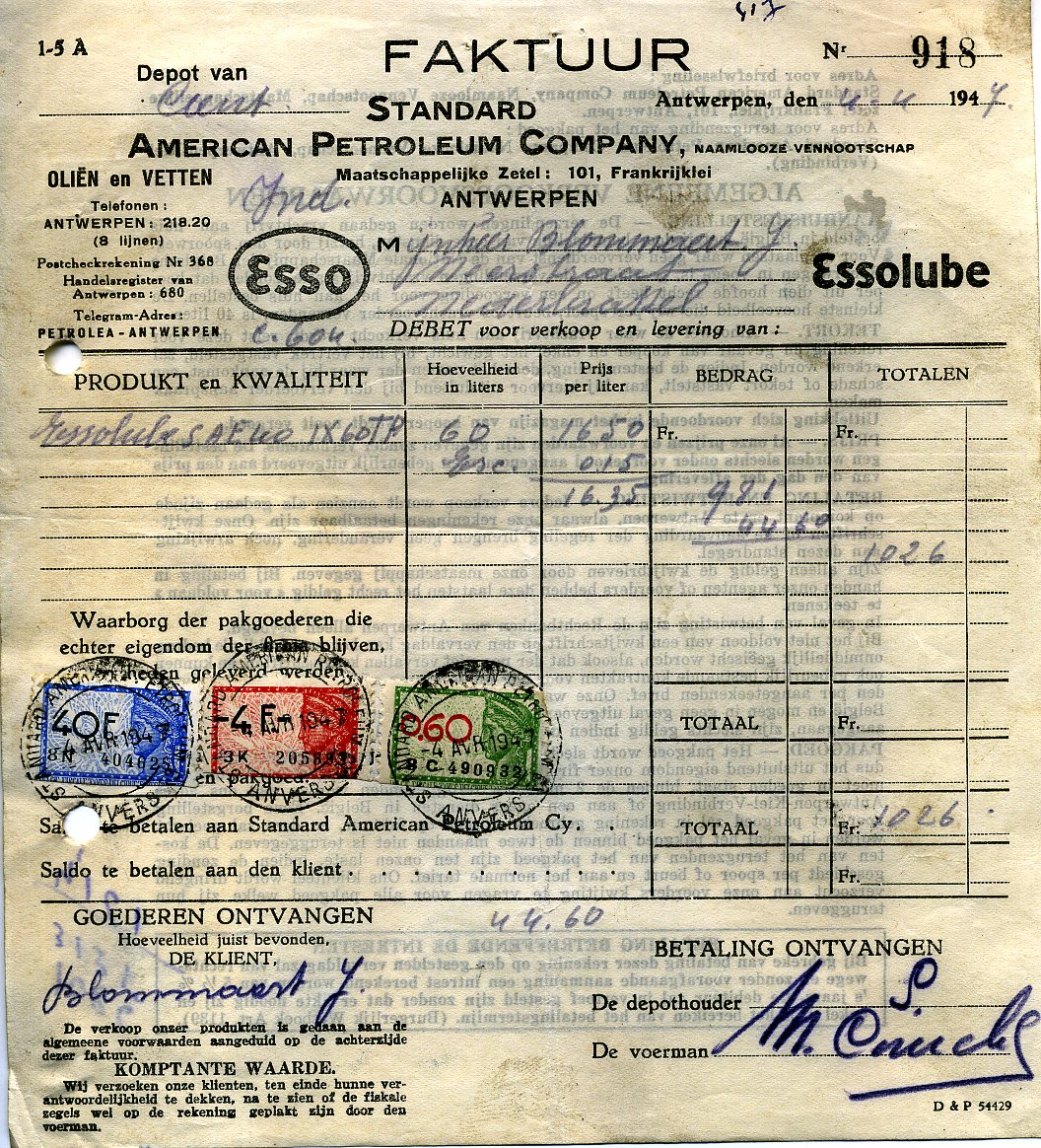

Invoice Invoice from Standard American Petroleum Company a...

Invoice from Standard American Petroleum Company a...Once the requisition goes through management approval, the purchasing team receives the order. At this point, a purchase order number is generated along with a request for the item. If the request is for a contractor a "statement of work order" will be attached. The purchase order numbers for both the product and service are then sent to the supplier.

In the electronic world, all invoices are sent to the mail/scan room. There they will be identified, prepared and analyzed for their validity to the accounting cycle. They are then time-stamped, sorted into doc type and batched. As they are batched, they are checked to make sure that they are invoices and not quotes or statements. That if the doc type is a travel and expense report that the correct backup is attached. If the item is...