Reporting Entities in New Zealand nowadays are required to provide a true and fair view when they disclose their financial reporting, namely, financial position, financial performance and cash flows. This requirement is not new; it can be traced down to the United Kingdom in 1844. As a colony, New Zealand followed this way. Because there is no legislative definition about the real meaning of the true and fair view since its appearance, the Companies Act 1993, in conjunction with the Financial Reporting Act 1993 reduced the concept's overriding position, and made it a supplement to generally accepted accounting principles (GAAP) since1993 due to ambiguousness and imperfectness. This change probably indicates the true and fair view need to be defined clearly and consummated with time. However, I still think it should remain as part of the regulatory and professional requirements for financial reporting in New Zealand not be replaced or removed.

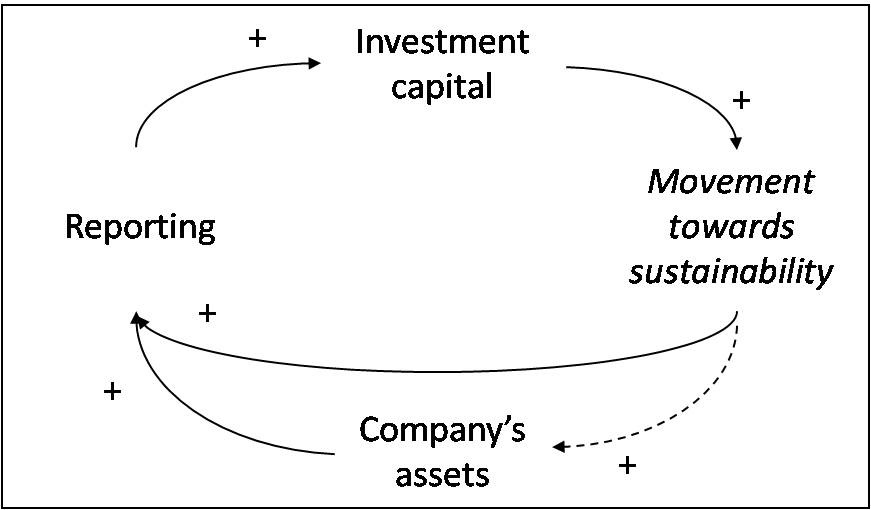

English: By incorporating sustainability investmen...

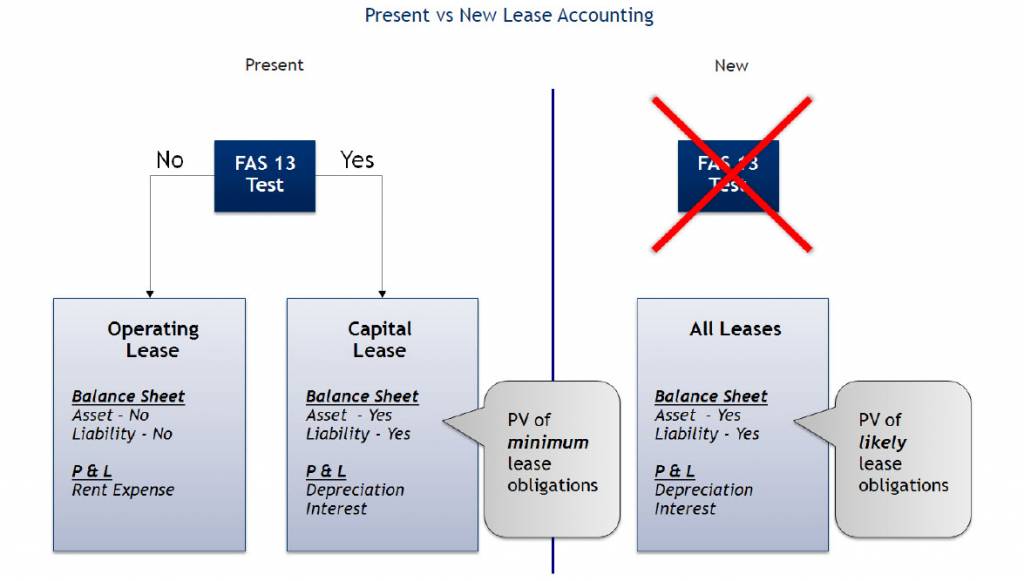

English: By incorporating sustainability investmen... English: Present vs. New Lease Accounting Standard...

English: Present vs. New Lease Accounting Standard... F9 software box with promotional pen

F9 software box with promotional penSince 'true and fair' has not been given an authorized definition, analysing the basic literal meaning of the concept is to be indispensable. One is the meaning of 'true' and 'fair' in this phrase. Do they signify the same thing? They both emphasize the nature of the concept that is the truth, although they might vary according to the changing situations and accounting environments. Most Australian directors and New Zealand auditors treat true and fair as equivalent in meaning. (Kirk, 2006, p.209) The other one is the relationship between 'true and fair', 'fairly reflect' and 'fairness presentation'. In New Zealand Preface, the terms 'fair presentation' and 'fairly reflect' have the same meaning as 'true and fair view' (NZ Preface, Para. 8, ICANZ, 2005).

These all try to focus on the substance of the concept instead of the form.

Furthermore, how is the inner relationship about the concept of...

Good

well structured and has a nice bibliography

0 out of 0 people found this comment useful.