The cost of a product under marginal costing or variable costing includes only the variable costs of making the product. The variable costs include direct material, direct labour and variable overheads. Variable costs per unit approximate the marginal cost of making another unit of a product. Selling price minus variable costs adds up to contribution. Contribution is the amount of money available to cover the fixed costs and afterwards to contribute to profit. The fixed costs are treated as period costs and are expensed in the period incurred.

Marginal costing can be used to assist in decision making in the following circumstances: acceptance of a special order, dropping a product, make or buy decision and to choose which product (mix) to produce when a limiting factor (resource) exists. The technique of marginal costing mainly concentrates on financial factors, for instance the company's objective to maximise profit or to create wealth.

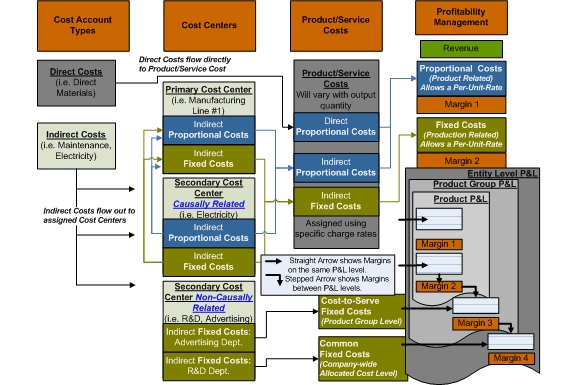

English: GPK Marginal Costing Structure Flow of Gr...

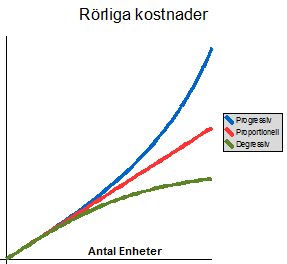

English: GPK Marginal Costing Structure Flow of Gr... English: Variable costs in swedish Svenska: Rörli...

English: Variable costs in swedish Svenska: Rörli... Average Variable Costs

Average Variable CostsBut other non-financial or commercial implications with long term character are largely ignored. If a company decides whether it should drop a product or not, it is necessary to consider commercial factors. If it stops producing a product because of its profitability, it might upset customers who have bought this product over years. And it may happen that they start buying their whole products from competitors. A company should not think immediately about dropping a product when the demand is too low, since it is short term thinking to let thousands of customers go away. It should rather think about exceeding the demand. Further on, the product to be dropped may be a complementary one to another product made by the company. The problems of scarse resources can be compared with those of dropping a product. If an enterprise decides to make an optimum product mix (=profit maximising product mix), it might be in the position of not having enough resources to make a product with a lower contribution. The same effects of dropping a product could be a consequence. The acceptance of an order might depend on non-financial factors as well. The firm should consider if it could sell the products itself under another (low cost) label. Furthermore a company must pay attention to its price in the primary market because the orderer might offer the product either for a higher or lower price. Make or buy decisions are difficult because outsourcing always jeopardizes the jobs of those currently working for the company and the quality of the job to be done. The firms' image and thereby its sales are put in danger, if it makes frivolous redundancies. Moreover, the company has to make sure that it gets the same quality of output for less money to justify the outsourcing.

In my opinion it is true that marginal costing ignores other relevant commercial factors. The contribution of a product on its own should not be decisive and is short term thinking. A company has to pay attention to customers, public and competitors as well. A long term strategy including financial and non-financial factors should be established to ensure a profitable and sustainable performance.

Marginal profit is the difference between a firm's...

Marginal profit is the difference between a firm's... Having a Nobel gas

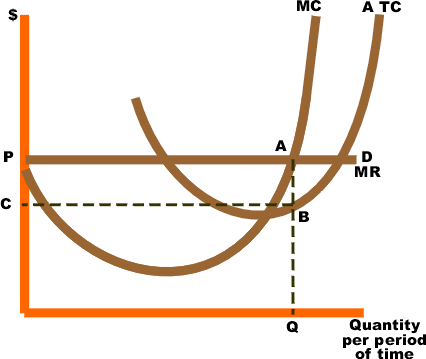

Having a Nobel gas Typical progress of marginal cost

Typical progress of marginal cost