Cost allocation is a method to determine the cost of services provided to users of that service. It does not determine the price of the service, but rather determines what the service costs to provide. It is important to determine the cost allocation of the services, in order to determine a justifiable fee/charge/tax for those services.

Included in cost allocation are direct, indirect, and incremental costs. Direct costs, or separable costs, are costs that are related to a single type of service and are related to one type of output or user such as, a sector-to-sector hand-off. Indirect costs, or common costs, are related to more than one type of service, such as, the physical en-route facility. Incremental costs change with the level of output produced. Incremental costs measure changes in output, e.g., differences in staffing levels or staffing costs at a facility that is based on traffic count.

Cost allocation is a factor that determines the cost of an activity.

Diagram of US Federal Government and American Unio...

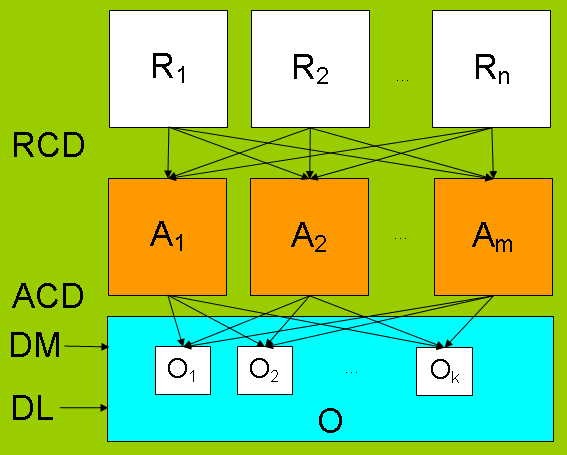

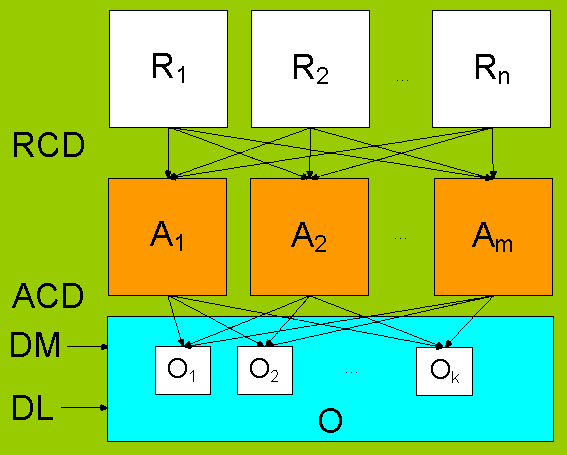

Diagram of US Federal Government and American Unio... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver...Cost drivers are analyzed as part of activity based costing and can be used in continuous improvement programs. They are usually assessed together as multiple drivers rather than singly. There are two main types of cost driver: the first is a resource driver, which refers to the contribution of the quantity of resources used to the cost of an activity; the second is an activity driver, which refers to the costs incurred by the activities required to complete a particular task or project.

We will answer the following questions from three different organizations:1)U.S. Army Corp of Engineer: Why does the US Army Corp of Engineers worry about cost allocations? Aren't they a branch of the US Federal Government? Why does it matter whether or not costs are allocated?A)The reason U.S. Army Corp of Engineer conduct a Cost Allocation...