Synopsis.

Historical Cost Accounting is a traditional valuation method as it reflects only on the past cost of the asset, however in the contemporary business environment companies must remain flexible and transparent. This belief has lead to the creation of several other valuation methods, due to word constraints I have focused primarily on Fair Value Accounting as an alternative to Historical Cost Accounting. Although Fair value accounting is a theoretically superior valuation methodology, there are several severe problems in its current application, due to lax regulations and ineffective methods of determining current values of non-current assets. These problems within Fair Value Accounting have ensured that most companies conservatively remain using Historical Cost Accounting.

What are Historical costs?

Historical cost is a generally accepted accounting principle requiring all goods or assets used in production to be valued by the expenditures actually incurred to acquire those goods or assets, however far back in the past those expenditures took place (System of National Accounts, 1993).

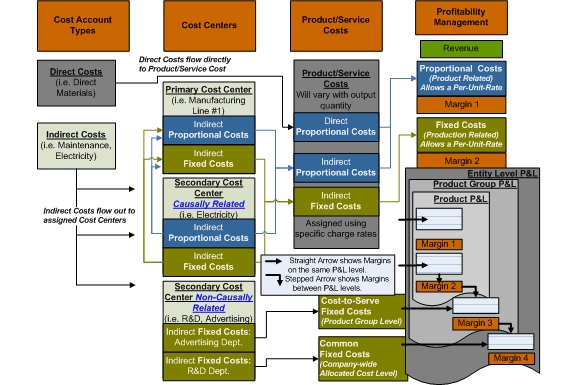

English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr... Photo tentatively identified as the information de...

Photo tentatively identified as the information de... Delavan’s Historic Brick Street Historical Marke...

Delavan’s Historic Brick Street Historical Marke...Valuing assets upon their original cost ensures valuations are objective, reliable and may be verified through invoices and documentation. Furthermore, accumulative depreciation ensures that the cost of the asset is spread throughout its productive lifetime. This method smooths out speculative fluctuations within Financial Statements to reflect comparable changes in company performance. The American Accounting Association (AAA 1936, p188) supported this view;

"...accounting is thus not essentially a process of valuation, but the allocation of historical costs and revenues to current and succeeding fiscal periods."

Criticisms of Historical cost Accounting

Historical cost method, over a period of time has been subject to many criticisms, especially as it tells the user the acquisition cost of an asset and its deprecation in the following years, but ignores the possibility that the current market value of that asset may be higher or...