Transfer Pricing

Chapter Outline

A. Cost Management Challenges - Chapter 19 provides four cost management challenges.

1. What is the primary purpose of establishing a transfer price policy?

2. What are four methods for setting transfer prices?

3. What is the significance of excess capacity in the transferring division, and what impact does that have on the transfer price?

4. Why might income-tax laws affect the transfer-pricing policies of multinational companies?

B. Learning Objectives - This chapter has five learning objectives.

1. Chapter 19 explains the purpose and role of transfer pricing.

2. The chapter explains how to use a general economic rule to set an optimal transfer price.

3. It explains how to base a transfer price on market prices, costs, or negotiations.

4. It discusses the implications of transfer pricing in a multinational company.

5. It discusses the effects of transfer pricing on segment reporting.

C. The chapter discusses the effects of transfer pricing on segment reporting.

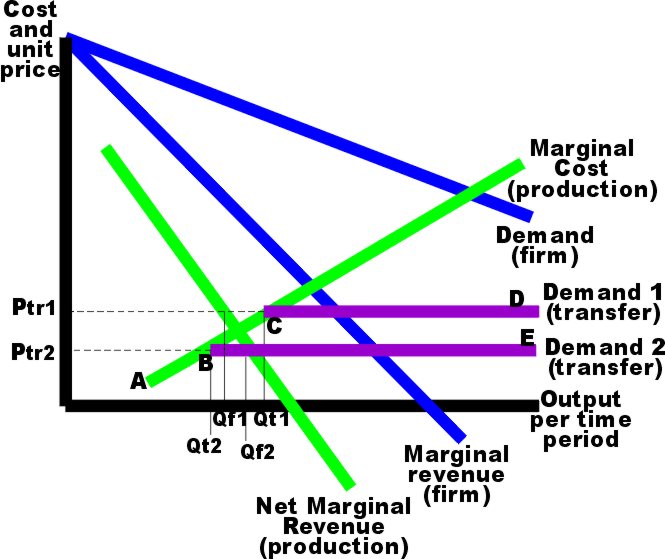

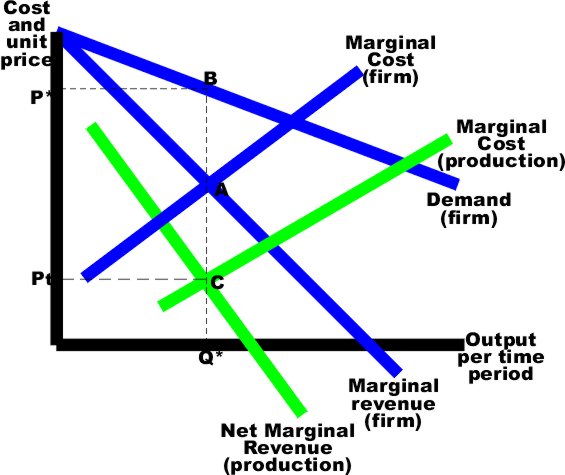

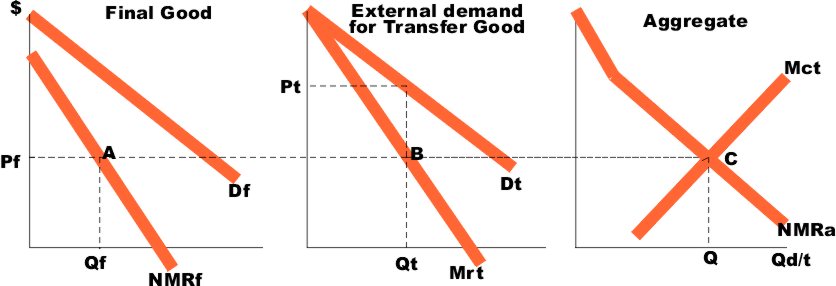

English: Transfer Pricing with a Competitive Exter...

English: Transfer Pricing with a Competitive Exter... English: Transfer Pricing with No External Market.

English: Transfer Pricing with No External Market. English: Transfer Pricing with an Imperfect Extern...

English: Transfer Pricing with an Imperfect Extern...A transfer price represents the amount charged when one division sells goods or services to another division within an organization. Transfer pricing is a challenge for cost managers because it represents an economic event that must be recorded in the accounting system. Deciding what the transfer price should be is the challenge. Transfers of goods and services within an organization do not impact the organization's profits as a whole organization. However, the buying and selling divisions' profits are affected by transfer prices charged. A high transfer price increases profits for the selling division and increases costs for the buying division.

If divisions are evaluated using ROI, residual income, or economic value added, then the transfer price can affect the performance of each division. This fact may motivate managers to pursue strategies for transfer pricing that are not congruent with organizational goals.