Cost Descriptors MemoTo: All Human Resource ManagersFrom: Jane Doe MBACC: Jim Jones CFODate: April 29, 2008RE: Cost DescriptorsAt the last meeting, it was apparent that our Human Resource Managers (HRM) lack the basic knowledge of the accounting cost descriptors terminology and concepts. The use of efficient cost accounting techniques in accordance with the generally accepted accounting principles (GAAP) regulations is mandatory for accurate income measurement and inventory valuation. It is imperative that all HRM understand how the organizations budget expenditures are affected by various operational costs. In order to facilitate effective forecast and business decision-making this memo will define the key costs terms referred to as fixed, variable, direct, indirect, sunk, marginal, total costs, actual, and opportunity costs. Examples of these cost terms will be given.

Cost accounting is mandatory for efficient management decision-making, planning, evaluation, and control through cost reduction and improved profitability. In the production of products and services, costs are assigned at each level of output and are tracking, recording and examined to determine the value of inventory, and the cost of products and services sold.

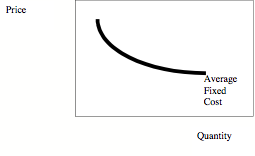

Average Fixed Costs

Average Fixed Costs English: Fixed Cost in swedish Svenska: Fast kostn...

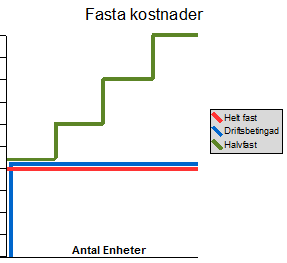

English: Fixed Cost in swedish Svenska: Fast kostn... English: Variable costs in swedish Svenska: Rörli...

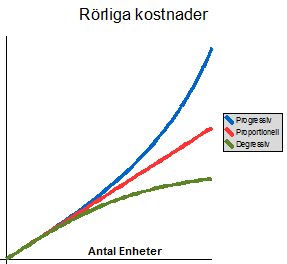

English: Variable costs in swedish Svenska: Rörli...These costs are reflected in the purchase of materials from outside suppliers and the combined cost of in house materials and the production process.

Fixed CostThe most basic accounting cost term is referred to as fixed costs (FC). FC are relatively constant operating costs that remain on the balance sheet or income statement from month to month regardless of the production volume or sales level (McConnell & Brue, 2004, chap 22. p.32). In the short run, FC are outside of a business manager's span of control. FC reflect the financial investment made during a business's long-term commitment, the business has fixed assets considered un-resalable. Examples of fixed costs include insurance premiums, interest on debts, loan payments, a portion of depreciation...